China’s Global Investment in 2024: Battery Bonanza Ends But Completed Investment Rebounds

Feb 18, 2025Thilo Hanemann, Armand Meyer, Danielle Goh

Newly announced overseas investment by Chinese companies dropped slightly in 2024 as new investments in battery manufacturing slowed sharply. However, completed investment trended up as Chinese companies moved ahead with capital intensive greenfield projects in manufacturing and extractive industries. New investment became more concentrated, with automotives, energy, and minerals and metals accounting for close to 80% of announced transaction value. Chinese investors continued to move away from North America and Europe with Asia as leading recipient and strong growth of new investment in Africa and the Middle East.

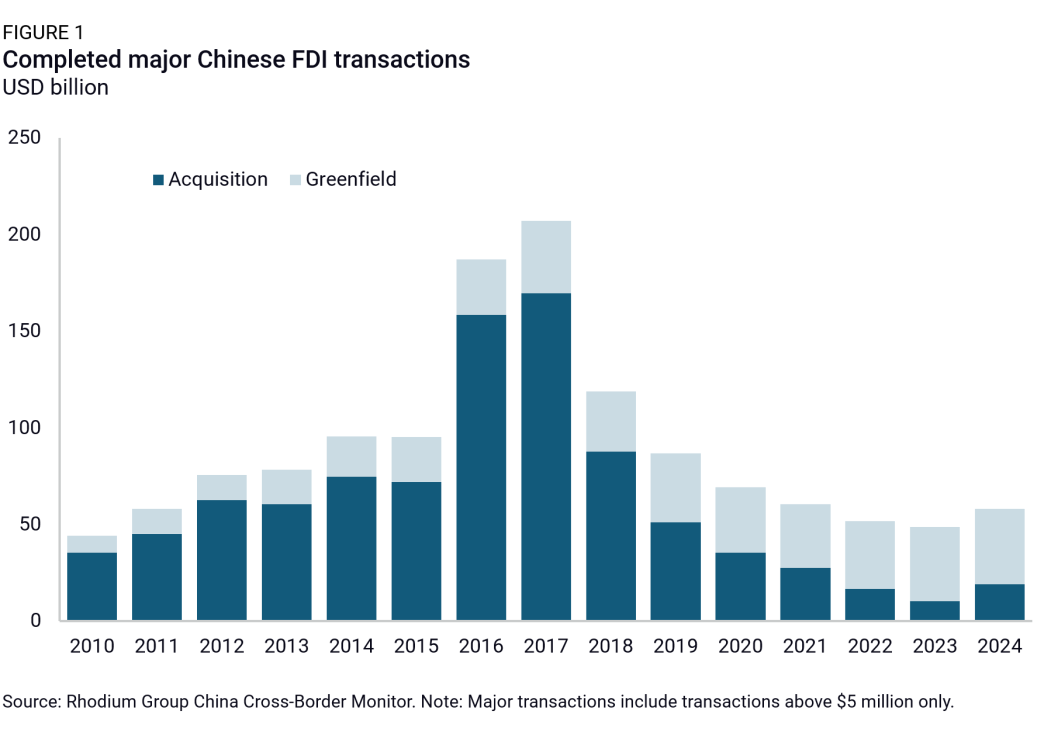

New battery investments fall, but completed investment rebounds

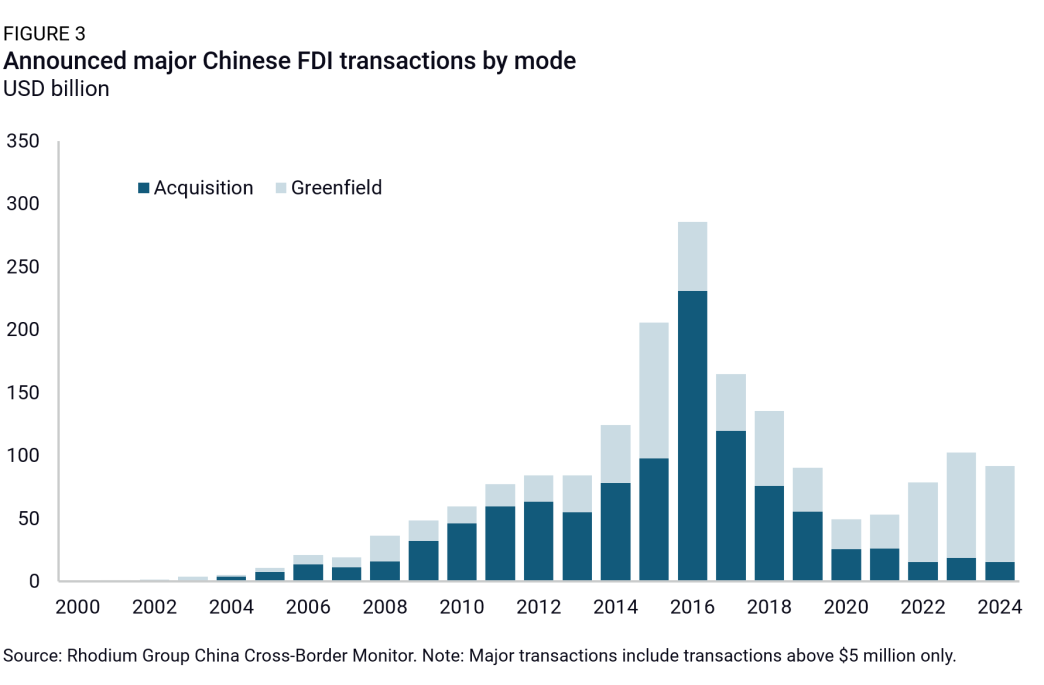

The value of newly announced Chinese FDI fell 10% in 2024. Most of this decline was driven by a sharp reduction of newly announced projects in the automotive sector, particularly in batteries, where investment value fell 70% compared to the 2022-2023 average. Despite this slowdown, 2024 saw the second highest newly announced overseas investment since 2020.

Completed FDI, on the other hand, was back to pre-COVID levels: In 2024, completed investment by Chinese companies totaled around $58 billion, the first year-on-year increase since 2017. Greenfield investments had already started recovering in 2023, while M&A saw its first increase since 2017, rising from $10.1 billion to $18.9 billion in 2024.

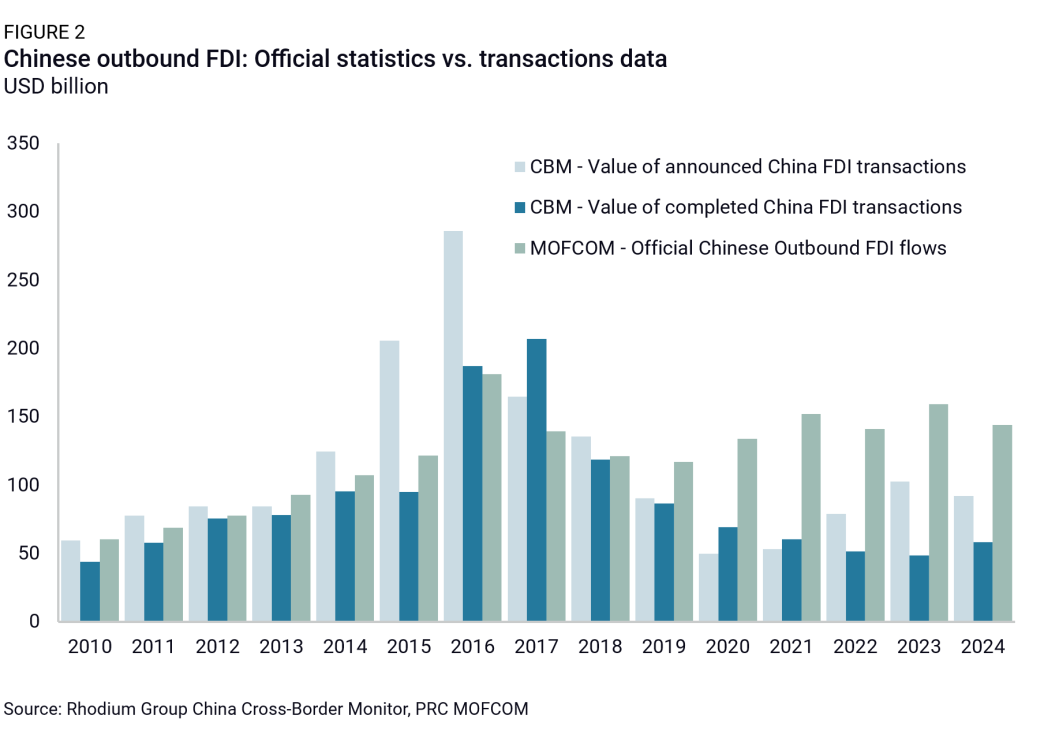

Verifiable investment remains lower than official statistics

Since 2019, the gap has widened between outbound FDI flows recorded by China’s government statistics and the value of identifiable FDI transactions by Chinese companies. This disconnect persisted in 2024. Official statistics from China’s MOFCOM show $144 billion of outbound FDI in 2024, suggesting that China’s OFDI has soared back to record levels last seen in 2016. However, our micro data on identifiable FDI transactions by Chinese companies does not back this up. While macro and micro data are not directly comparable, the extent of the discrepancy suggests that a significant portion of China’s reported OFDI does not represent genuine outbound FDI in global real economy operations. Instead, it reflects round-tripping and other financial flows related to offshore operations by Chinese banks and state-owned firms as well as funds exiting China via the FDI channel that would more appropriately be classified as portfolio investment (e.g., households diversifying wealth) in an economy without capital controls (for more context, see The Next Generation of China’s Outbound Investment).

Greenfield FDI in manufacturing and mining drives new investment

Greenfield FDI remained the dominant mode in 2024, accounting for more than 80% of the total transaction value. Capital intensive projects such as oil refineries, mines, and battery factories drove that trend, but manufacturing greenfield OFDI remained elevated in other industries as well. The number of M&A transactions remained low (165) but a rise in middle-market deals pushed the average investment value to $133 million, returning to 2017 levels.

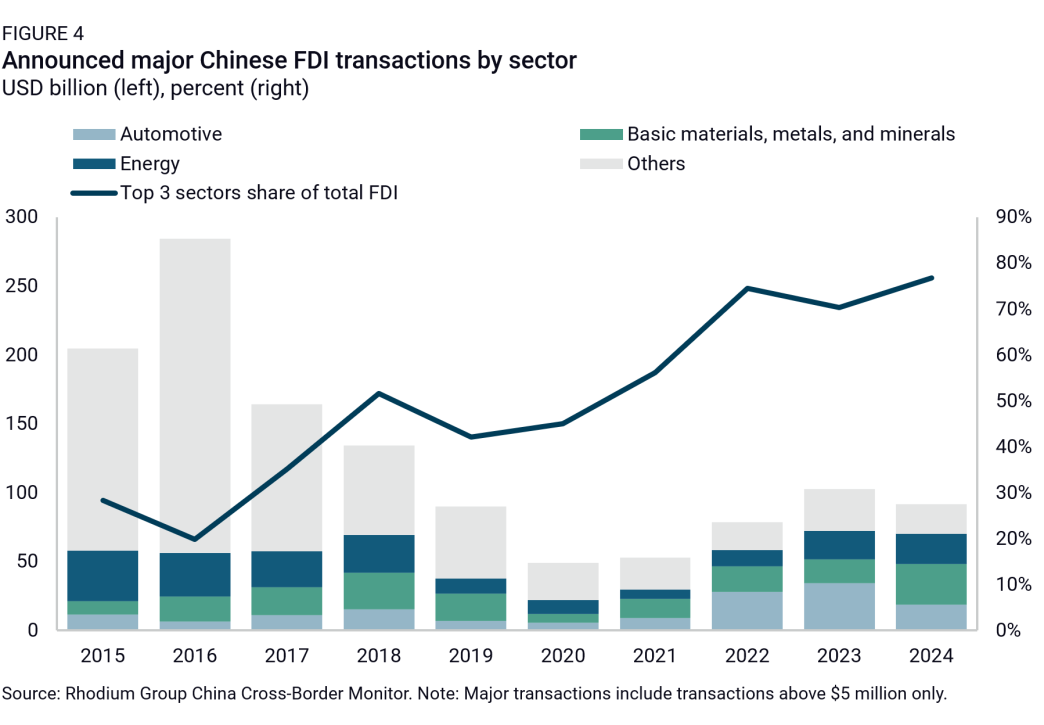

China’s outbound investment becomes more concentrated

Three sectors—automotives, basic materials, and energy—have dominated Chinese outbound FDI since 2020, collectively accounting for a peak of 77% of total FDI in 2024. In 2024, the automotive sector lost the pole position with only $18.9 billion of newly announced investments, the lowest since 2021. The sharp slowdown is the result of fewer newly announced investments in battery factories. Only 25 new battery transactions worth $7.4 billion were announced in 2024, compared to an average of 48 worth $23.8 billion over the previous two years. New EV assembly plants and parts manufacturing continue to thrive, but they don’t make up for the drop in battery investments. Basic materials took the top spot in 2024 with $29.3 billion of new investments, the second highest figure since 2018. Energy ranked second with $21.8 billion, its highest level since 2019. Investments in renewable energy equipment and power generation accounted for 64% of the total value.

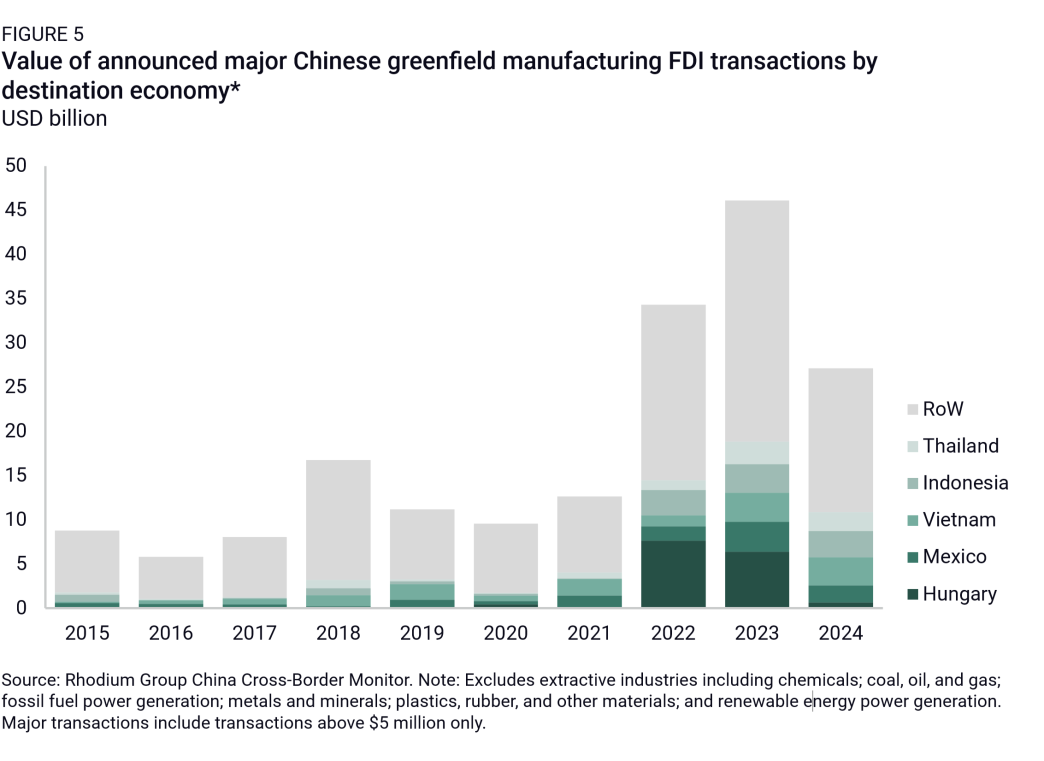

Chinese companies continue to build manufacturing supply chains outside of China

Chinese greenfield manufacturing FDI fell 44% because of a sharp drop in new battery projects, but investment in other industries remained robust. Even though auto investment halved, the sector remained the top recipient, driven by EV manufacturing and a surge in small car parts plants. Most other sectors maintained momentum, with renewable energy equipment investment rising 45% year-on-year. Asia remained the primary destination for outbound manufacturing greenfield FDI, but other regions, including MENA, experienced rapid growth. In contrast, the number of new project announcements in Mexico are falling back to pre-COVID levels, as investors adopt a wait-and-see attitude in response to US trade policy uncertainty.

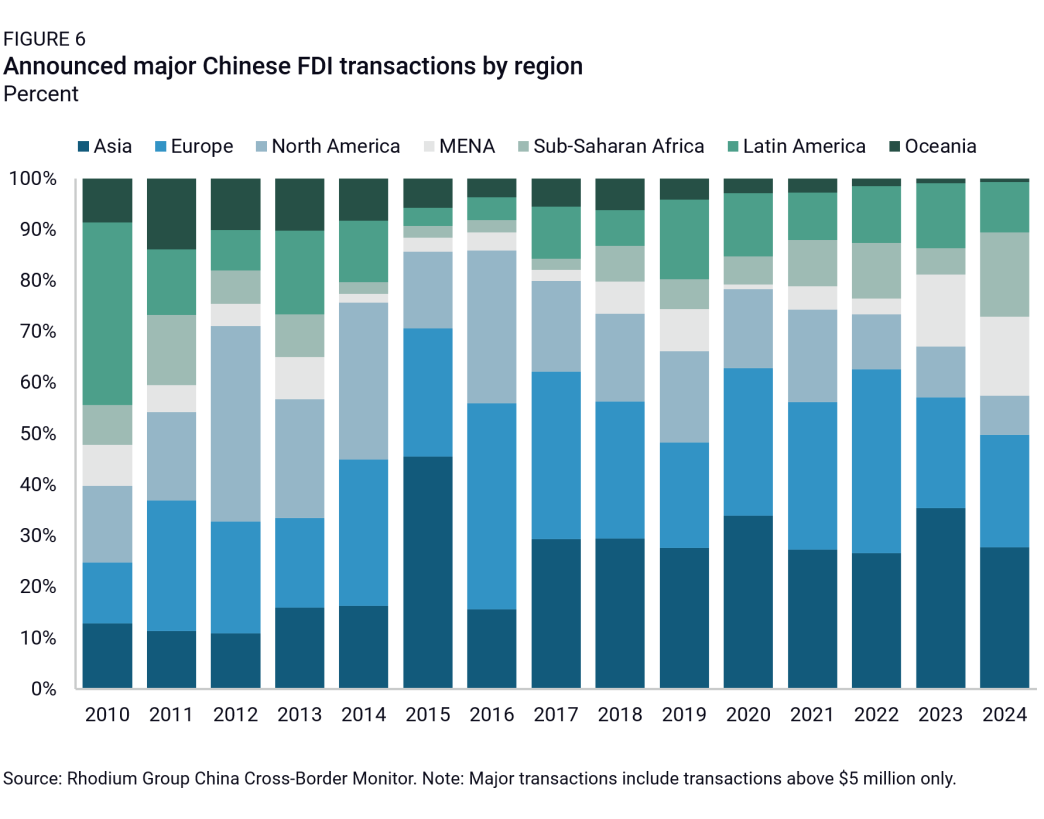

China’s global FDI footprint continues to diversify geographically

For the sixth year in a row, Asia was the top destination for Chinese outbound investment, despite a 30% year-on-year drop. New investments in Europe declined for the second consecutive year and continued to shift from Western Europe to Southern and Eastern Europe, with Serbia and Spain being top destinations in 2024. North America’s role continued to shrink with only $7.1 billion or 7.7% of total announced investment. Combined Chinese investment in North America and Europe dropped to the lowest level since 2010. On the other hand, emerging markets saw a greater share of total Chinese investment. Africa and the MENA region both recorded their highest-ever levels of announced Chinese FDI transactions in 2024. Chinese FDI in Sub-Saharan Africa reached an all-time high of $15.2 billion, representing 16.5% of newly announced investments in 2024.

Outlook for 2025

The structural drivers of greater Chinese outbound investment in manufacturing and extractive industries will likely remain in place. Although China may see some cyclical economic improvement this year, uncertainty about its long-term outlook remains. As a result, Chinese companies will be eager to expand their revenue from overseas markets. Growing trade barriers and supply chain security concerns will make it increasingly difficult to defend and grow market shares abroad through exports—pushing companies to instead grow their overseas presence through FDI. Low and especially middle-income economies will remain a focus as North America and Europe become more saturated and less accessible. A more volatile external environment and policy guidance from Beijing to minimize reliance on unreliable foreign entities will incentivize greater equity investment in overseas upstream energy and basic materials assets. While these drivers remain in place, Chinese investors have to navigate persistent political headwinds at home and abroad, which will keep outbound investment from returning to levels seen during boom years 2014-2017.