After years of slowing outbound investment, Chinese companies are again expanding abroad. But this new generation of China’s overseas investment has very different objectives and destinations than in the previous decade.

After years of slowing outbound investment, Chinese companies are again expanding abroad. But this new generation of China’s overseas investment has very different objectives and destinations than in the previous decade. Rhodium Group’s new China Cross-Border Monitor (CBM) tool tracks the changing global footprint of Chinese corporations. This note summarizes the contours of China’s next-generation outbound investment and discusses the implications for business and policy leaders.

The slowdown of Chinese outbound investment since 2016 has been more pronounced than suggested by official data: While Beijing’s statistics show stable outbound foreign direct investment (OFDI) patterns in the past five years, transactions data suggest that outflows have dropped to only a fraction of previous highs. Official data includes significant “phantom” FDI driven by financial considerations, not real economy investment.

Outflows have rebounded after COVID-19 but remain far from previous highs: After hitting a bottom in 2021, announced outbound FDI by Chinese firms has rebounded in the past two years. However, investment levels are nowhere near previous highs if controlled for rumored transactions without specific location and scope.

New OFDI is likely to be closer to home and driven by organic internationalization efforts of mature companies: Chinese outbound investment is increasingly driven by the organic expansion of mature private companies with global ambitions rather than large one-off acquisitions. Investment is more concentrated on emerging markets than G7 economies, with a noticeable shift toward Asia.

Business and policy leaders will have to grapple with new opportunities and risks: This next generation of Chinese outbound investment provides opportunities for governments and businesses but will also create novel national and economic security concerns. Managing these risks may require governments to update existing policy regimes such as investment reviews, trade policy, industrial policy, anti-subsidy instruments, and supply chain security rules.

The boom and bust of China’s outbound FDI

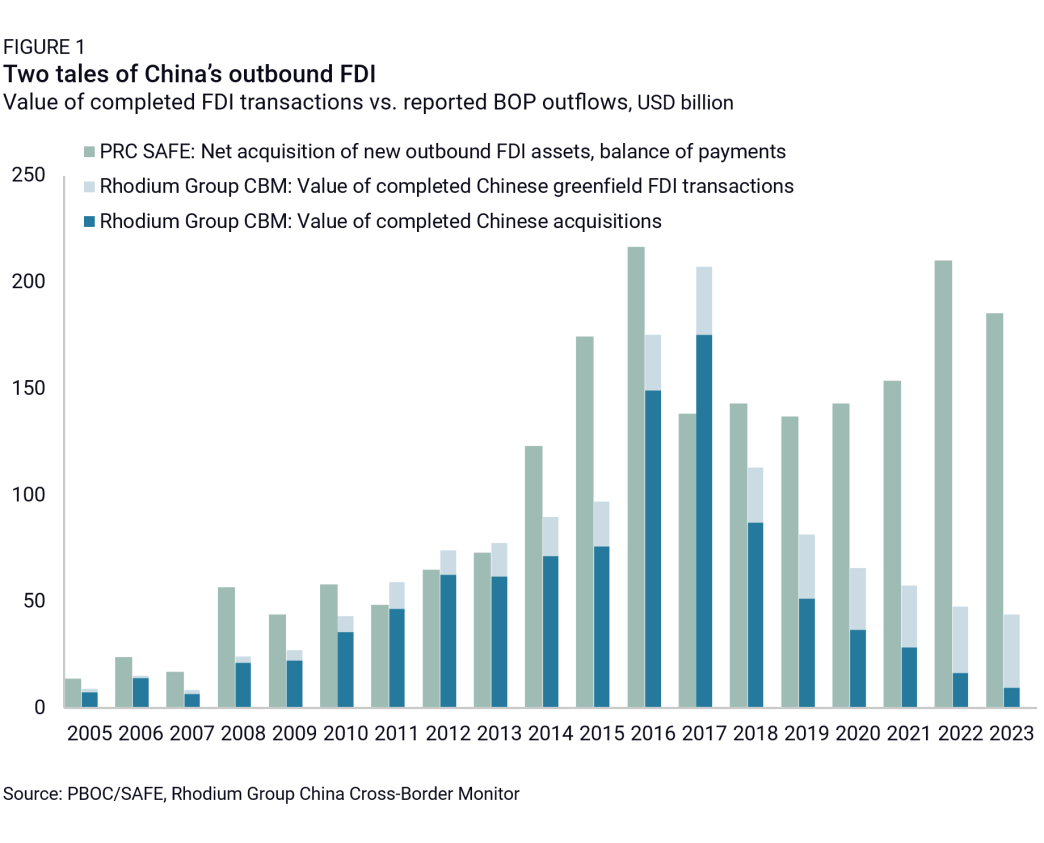

Outbound FDI by Chinese firms was barely existent in the early 2000s but started to grow in the early 2010s as firms seized opportunities arising from the global financial crisis to internationalize and diversify globally. China’s outbound FDI entered its boom phase after Beijing loosened investment approvals in 2014, driving the value of annual FDI transactions to more than $200 billion in 2016 (Figure 1).

This level of outflows triggered anxieties about capital flight and Beijing hit the brakes, re-tightening capital controls in 2017. Efforts to de-leverage the financial system and anti-corruption campaigns that affected many prominent outbound investors—HNA, Anbang, and Fosun, to name a few—caused additional headwinds. The 2014-2016 wave of Chinese capital also triggered a re-assessment of national security and economic risks in recipient nations, leading to higher regulatory barriers for Chinese investors in technology sectors, critical infrastructure, and other sensitive areas.

As a result of these policy changes at home and abroad, Chinese outbound FDI dropped after 2016 and 2017, but the extent and trajectory of this slowdown is contested. China’s official balance of payments (BOP) statistics show annual outflows dropping by about 30% in 2017 and staying roughly flat thereafter at an average of $150 billion annually. Datasets that track verifiable real economy FDI transactions show a much sharper slowdown. Rhodium Group’s CBM data shows that the annual value of completed FDI transactions by Chinese companies dropped in half from $204 billion in 2017 to an average of $97 billion in 2018 and 2019. The COVID-19 pandemic and China’s draconian zero-COVID policy further crippled the internationalization ambitions of Chinese firms, dragging average annual investment down to an average of $45 billion from 2020 to 2023.

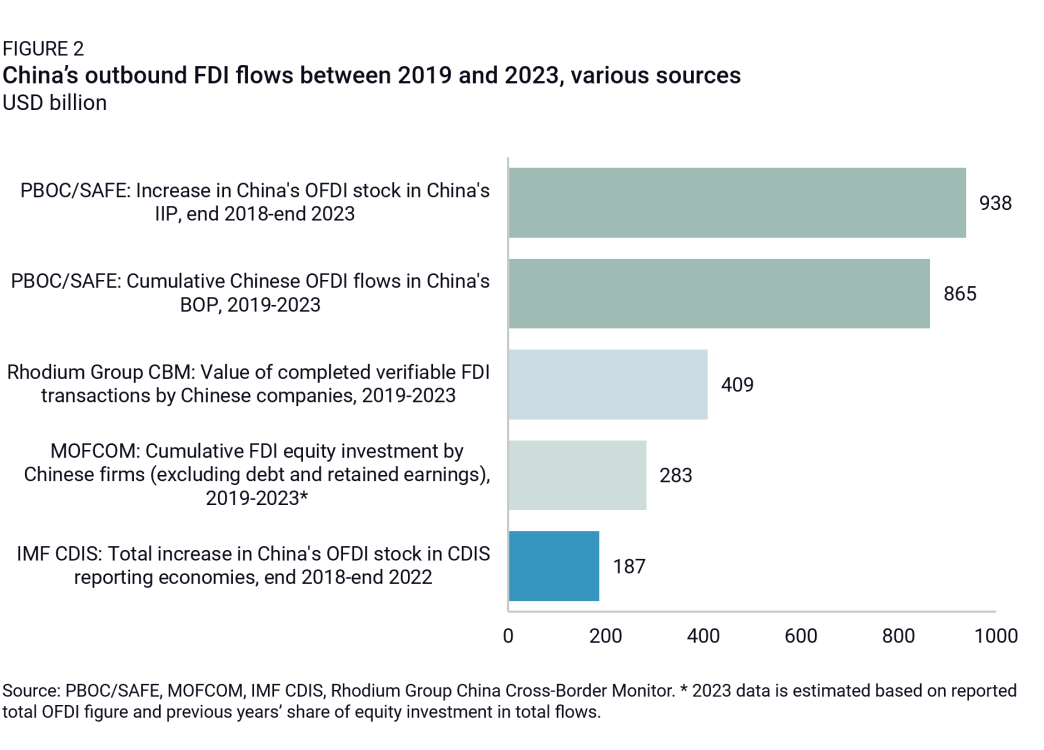

The resilience of China’s OFDI since 2018 as reported by SAFE is not only out of line with CBM transactions data, but also other available data points (Figure 2). Compared to almost $1 trillion of new OFDI assets reported by China, the roughly 115 countries that participate in the IMF’s Coordinated Direct Investment Survey (CDIS) reported only a total of $187 billion of new FDI from China since 2018. China’s Ministry of Commerce (MOFCOM) reports only $283 billion in new equity FDI investments by Chinese firms abroad in the same period, suggesting that more than two thirds of official outbound investment flows were retained earnings, debt, and intra-company transfers.

Taken together, these data points suggest that a significant share of China’s reported OFDI in recent years is not “real economy” investment, but rather reflects Chinese firms stashing away earnings from exports and other international activities in offshore USD accounts. It could also be partially a result of deliberate attempts by the PBOC to use state-owned banks, enterprises, and investment vehicles to recycle inflows from record trade surpluses into FDI assets instead of inflating China’s official reserve holdings, especially during the period of strong capital inflows from 2020-2022. The problem of “phantom FDI” is certainly not unique to China, but it is exacerbated by Chinese capital controls, the historical role of Hong Kong as global gateway for Chinese companies, and the lack of transparency around official government assets, adding to the many inconsistencies already identified with China’s external economic statistics.

The post-pandemic rebound

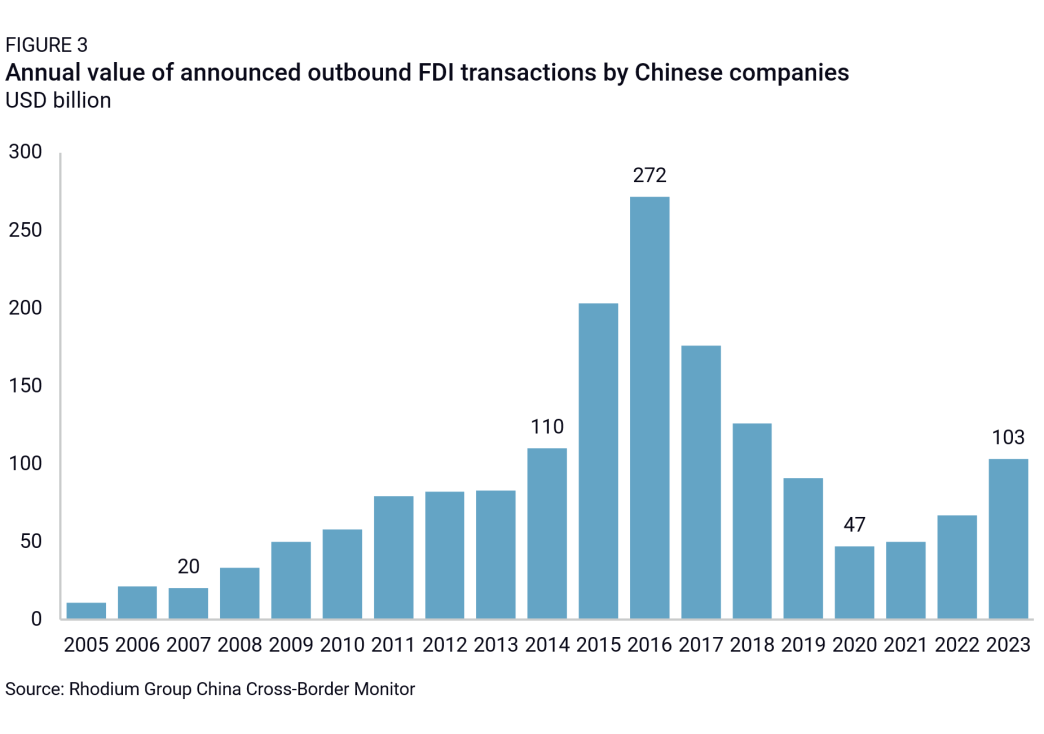

While investment had been in a tailspin since 2017, our CBM dataset on announced FDI transactions by Chinese companies shows a rebound in new activity since 2022. Newly announced FDI values bottomed out in 2020 at $47 billion and increased to $67 billion in 2022 and $103 billion in 2023 (Figure 3).

This represents a substantial recovery, but investment remains far from record highs if we exclude rumored projects that have no disclosed scope, location, or other operational details of the project. The value of announced FDI transactions in 2023 is still less than half of what it was in the peak year of 2016. It is also important to note that, based on our historical data, only about two thirds of the initially announced investment value eventually materializes. Many of the newly announced projects—such as manufacturing facilities in the electric vehicle industry—will take years to be completed and their trajectory hinges in part on how local political dynamics play out.

Emerging patterns of next-generation Chinese OFDI

The patterns of Chinese OFDI since the pandemic bottom show marked differences from the trajectory of the previous decade, giving us a glimpse of what the next generation of Chinese outbound investment might look like. Three trends stand out: A more significant role for greenfield projects, a geographic shift away from high-income economies toward emerging markets, and more diverse internationalization efforts across value chain segments instead of opportunistic acquisition of trophy assets.

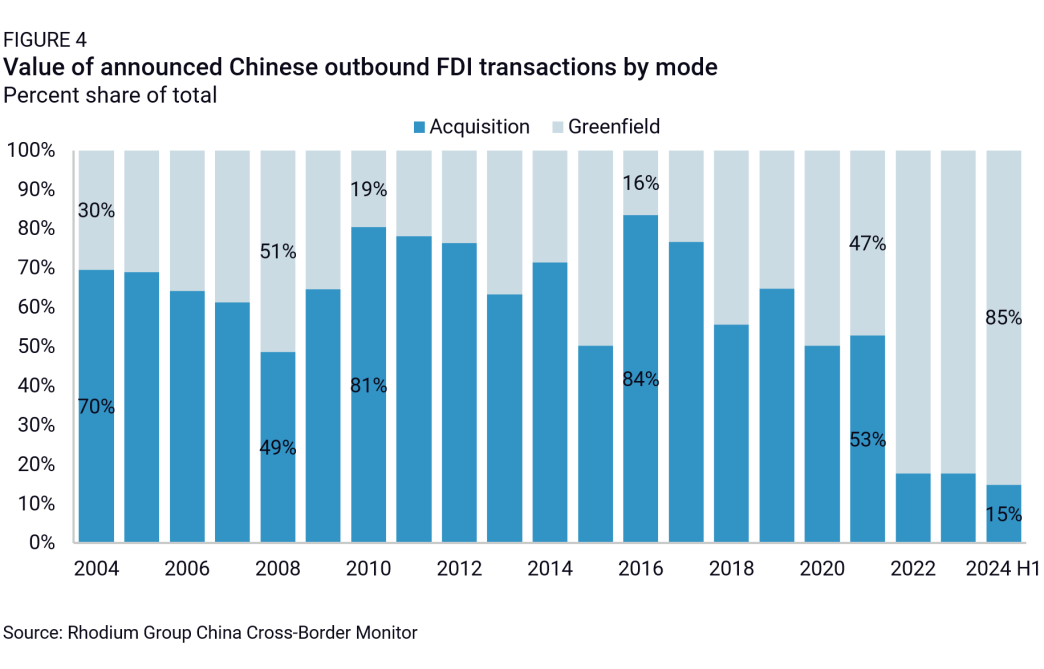

First, over the past eight years, the entry mode of Chinese investors has flipped from acquisitions to greenfield projects. For most of the past two decades, Chinese outbound investment was dominated by mergers and acquisitions (M&A). From 2005 to 2021, M&A accounted for 70% of the value of newly announced OFDI transactions by Chinese firms. Since 2016, M&A activity by Chinese firms has declined significantly, bringing down the relative share of M&A in total announced investment from 85% in 2016 to 50% in 2021 and only 15% in the first half of 2024 (Figure 4).

This shift is driven by a significant slowdown of M&A activity as well as a greater appetite for capital-intensive greenfield projects. M&A activity came under pressure due to greater regulatory hurdles at home and abroad. In 2016, Chinese companies announced M&A transactions worth $240 billion, or an average of $20 billion per month. In 2023, they announced $20 billion of M&A deals during the entire year. On the other hand, greenfield FDI was relatively low in previous decades as Chinese firms mostly served overseas markets through exports. Growing trade barriers abroad, pressure to diversify supply chains, and the growing competitiveness of Chinese firms in advanced industries like automotives have changed that equation. This has led to a boom in greenfield FDI in capital-intensive sectors such as EV batteries, pushing the values of greenfield FDI to 80% of total investment since 2022. While M&A activity may recover in coming years, greenfield FDI will remain a more important driver of China’s overall outbound investment than in the previous decade.

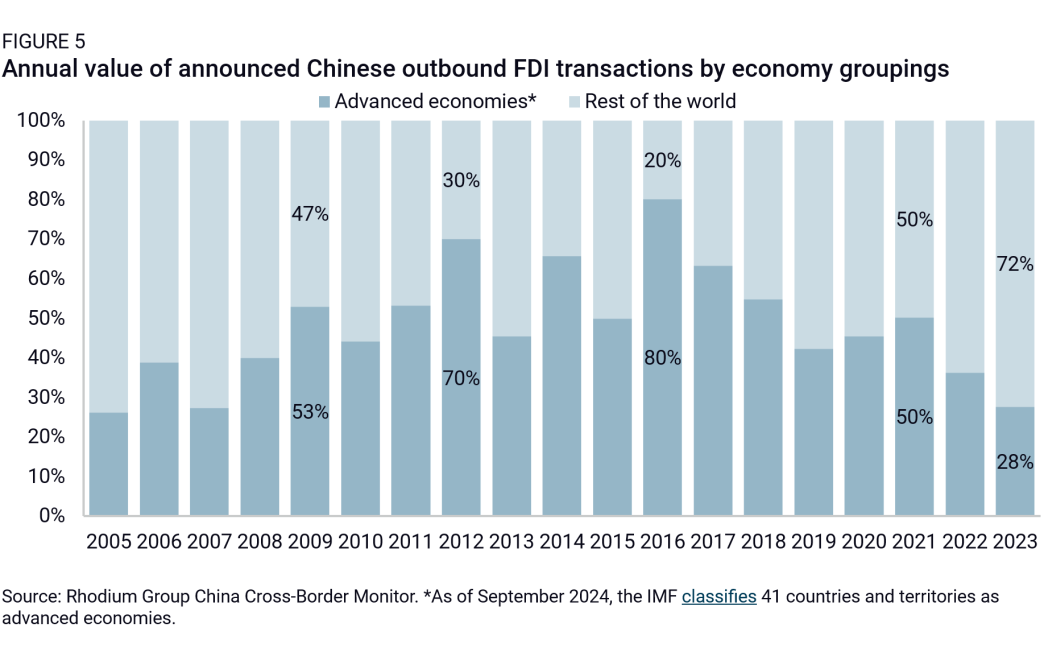

Second, Chinese outbound FDI has been shifting away from advanced economies toward Asia and emerging economies. During the decade of booming Chinese outbound FDI, more than half of investment was destined for Europe and North America, which are safe haven economies with a mature asset base and also China’s largest export markets. In 2016, close to 70% of total announced investment went to these economies. In the past five years though, flows to North America have contracted sharply, in no small part because of Chinese restrictions on “irrational” overseas investments in sectors such as real estate or entertainment. Flows to Europe are holding up slightly better, but the combined share of North America and Europe dropped to less than half of total annual investment. The biggest relative winner was Asia, which has become the largest recipient of Chinese outbound FDI since 2017. Vietnam, Malaysia, Indonesia, and Singapore have all seen at least $1 billion in investments in 2023 and 2024 as Chinese firms invest in automotive, real estate, and metal and mineral assets. Africa, Latin America, and the Middle East have also become more significant recipients of Chinese capital in the past five years.

Third, Chinese companies have become more mature and are using outbound FDI to truly internationalize their business presence instead of acquiring strategic assets or safe haven assets. During the first big wave of outbound investment, Chinese firms were eager to acquire strategic assets to increase their own competitiveness, starting with stakes in oil and gas and other upstream natural resource assets. This acquisitiveness later moved toward technology assets in sectors like automotive parts and semiconductors, trophy assets like the Waldorf Astoria, and consumer brands like IBM personal computers, Club Med, and Weetabix. Now, Chinese firms are increasingly shifting their focus from strategic asset acquisition to exploiting their own assets and advantages and gaining a foothold in new markets.

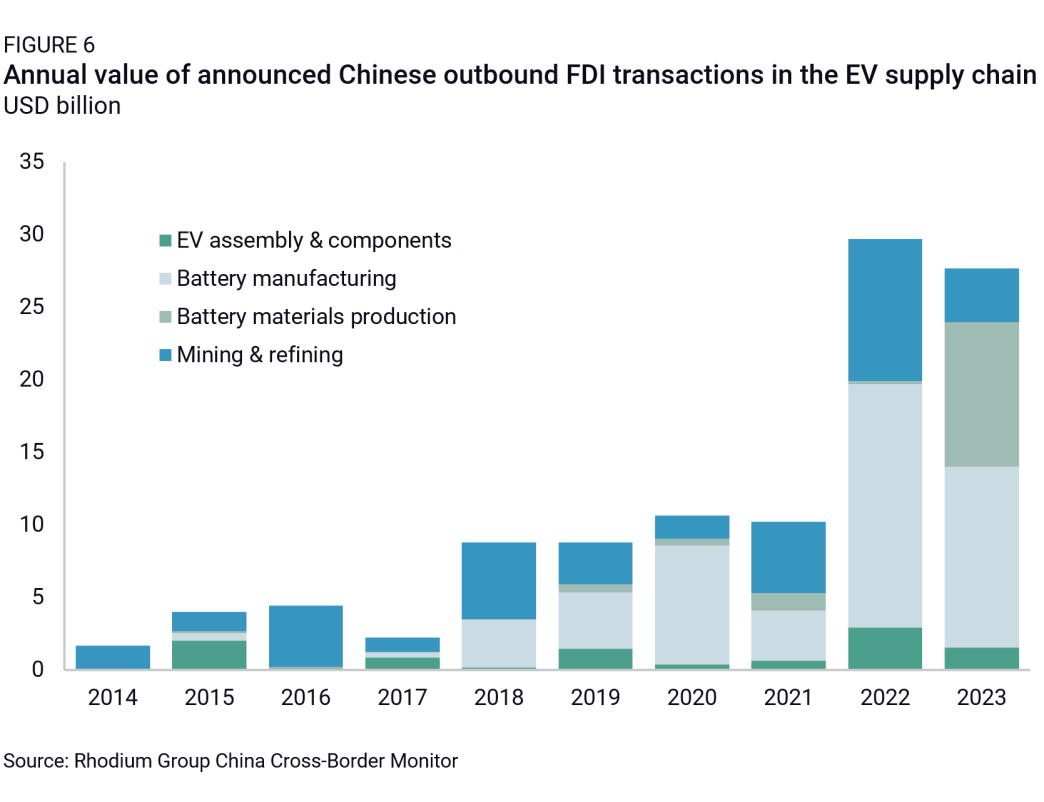

Investment patterns in the automotive industry exemplify these new trends (Figure 6). For the longest time, investment was relatively small and mostly concentrated on acquiring stakes in upstream resources. Today that picture has changed. Chinese firms such as BYD have built up an advantage in technology and scale and are now leveraging FDI to exploit these advantages and gain market share in overseas EV markets, mirroring the move of foreign automakers into China three decades ago. FDI is driven by both market logic—establishing local manufacturing, sales, and service operations for more complex goods—and political logic as tariffs and implicit and explicit local content requirements encourage the localization of production in major markets.

Implications for business and policy leaders

The previous wave of Chinese outbound FDI led to a meaningful overhaul of policy regimes across the globe. Foreign investment screening processes were strengthened to address national security risks, new tools like the EU’s Anti-Subsidies Instrument were drawn up to address economic security and level playing field concerns, and some governments moved to exclude Chinese companies altogether from sensitive sectors such as telecommunications services and other critical infrastructure. The new era of China's outbound investment will bring a different set of risks and opportunities that policy and business leaders must grapple with.

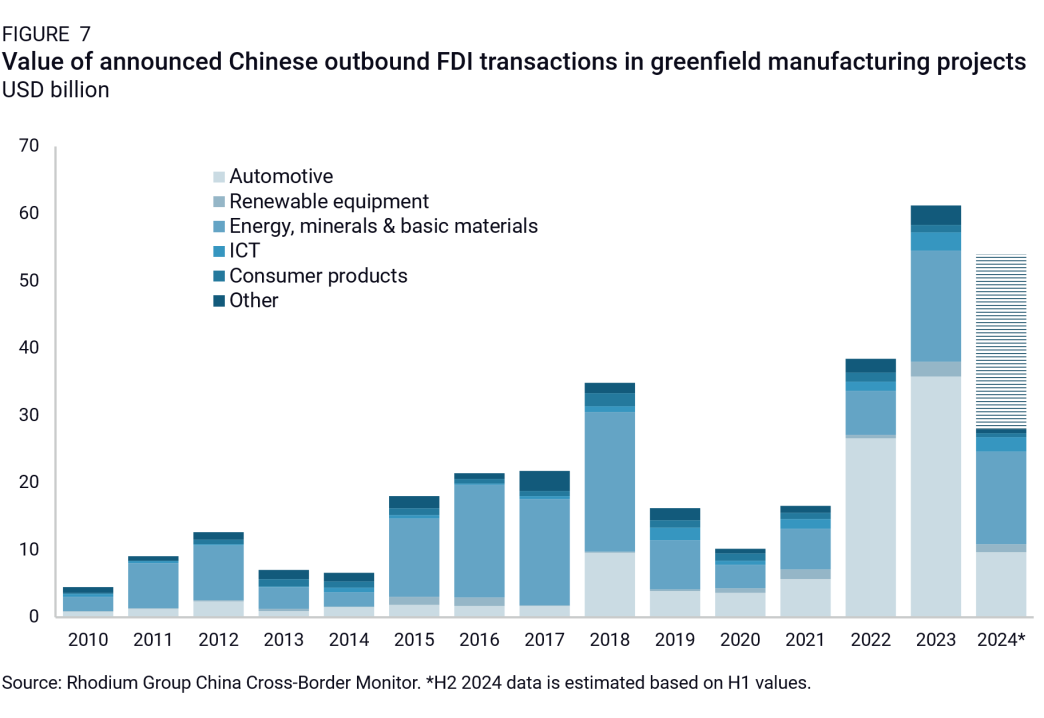

One of the biggest opportunities for national and local governments is for Chinese FDI to create local jobs and, ironically, reduce reliance on China as a manufacturing base. In past decades, China used inbound FDI to build up the largest manufacturing base in the world. Now Chinese outbound FDI in overseas manufacturing facilities is booming like never before (Figure 7), which is creating manufacturing jobs locally and may help reduce the world’s reliance on “Made in China” products. Governments are already pursuing Chinese capital to boost priority sectors—for example, Hungary’s efforts to build out its automotive industry or Malaysia’s efforts to expand semiconductor manufacturing. FDI also allows Chinese firms to enter new markets they cannot serve through exports, bringing additional competition to incumbent producers, which could result in lower prices and more choices for consumers. Finally, a growing global base of FDI assets will give Chinese companies a more tangible stake in the global economy and thus may increase the cost for Beijing to make policy decisions that would lead to more radical economic decoupling between China and democratic market economies.

At the same time, new risks must be considered and managed. Countries may have to further re-think their national security-focused investment screening processes to account for the fact that greenfield FDI has become the dominant entry mode of Chinese capital. The emergence of truly transnational Chinese companies means that investment screeners must now consider the entire global footprint of a Chinese acquirer—including other affiliated Chinese companies—to adequately evaluate the potential security concerns related to an individual investment.

China’s next-generation OFDI will especially require novel approaches to managing economic concerns and economic security risks. Chinese FDI is now geared toward taking market share in overseas markets, so incumbent companies will increasingly find themselves in competition with Chinese firms at home and in third markets. This competition will put governments in the position of weighing their free market principles against legitimate concerns that subsidies and other elements of unfair competition could wipe out incumbent companies in key sectors of the economy. The global expansion of Chinese EV makers will be the first test of how well-equipped governments are to navigate this challenge. Another important area is supply chain security. Governments are spending significant resources on nearshoring or friendshoring efforts but will have to be careful that these efforts do not end up inadvertently creating new vulnerabilities through investing in suppliers at home or in third countries that are already controlled by a Chinese investor.

Finally, growing Chinese outbound FDI will take strategic competition with China for economic influence in the Global South to the next level. In the past, China’s presence in emerging economies often took the form of Chinese policy banks financing infrastructure built with Chinese workers. Now Chinese companies like BYD are building “sticky” FDI operations that create local employment, pay local taxes, and offer attractive products at attractive prices in local markets. As a result, governments that are eager to counter China’s economic influence in emerging economies face a tougher challenge. They now must compete with not only state-backed financing from Beijing, but also with a new crop of mature Chinese multinationals promising a broader set of local economic benefits.