No Tariff Bump Yet for Chinese Outbound FDI: Q1 2025 Update

May 08, 2025Thilo Hanemann, Armand Meyer, Danielle Goh

Chinese outbound FDI held steady in Q1 2025 compared to previous quarters. Greenfield investment continued to dominate but new investment in offshore manufacturing facilities remained lower than in 2023/2024 as Chinese investors await greater clarity on tariffs. Despite a slowdown of new manufacturing projects in ASEAN, Asia remained the top destination of new investment, followed by Sub-Saharan Africa and Europe. Energy, basic materials, and infrastructure were the top investment sectors while automotive investment continued to slow as investments along the EV supply chain lost further steam.

Investment momentum

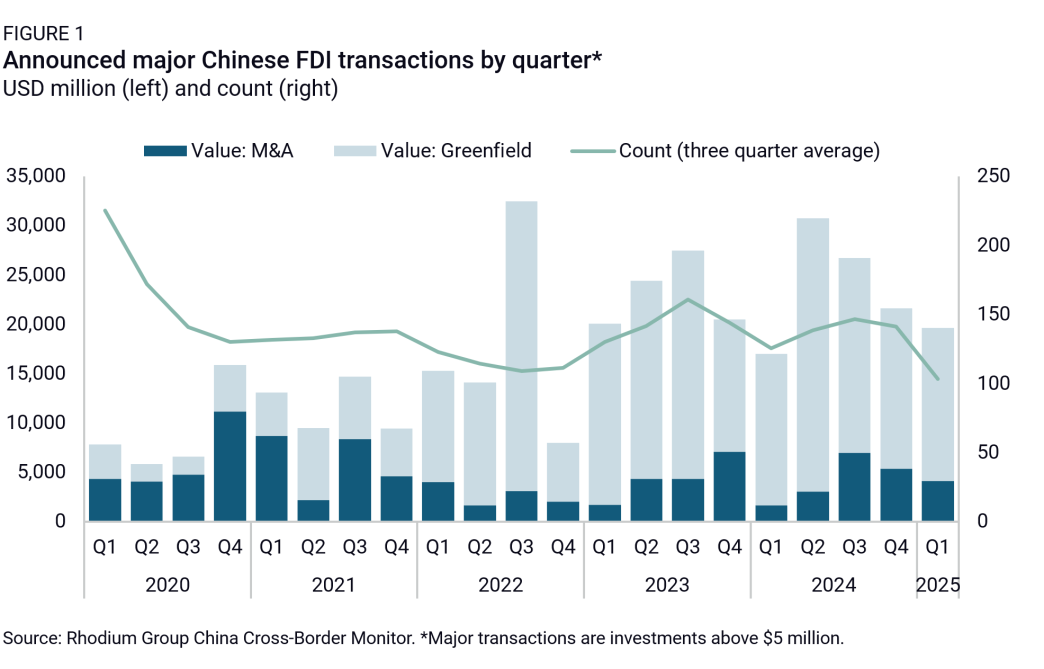

Updated China Cross-Border Monitor (CBM) data shows 90 major FDI transactions by Chinese companies in Q1 2025 totaling an estimated $19.7 billion. That represents a modest decline compared to previous quarters, but a 15.7% increase compared to Q1 2024.

Greenfield investment decreased by 4.6% from the previous quarter to $15.5 billion, accounting for 79% of total investment. Six transactions worth more than $1 billion were announced. The largest was a $4 billion green hydrogen project in Nigeria’s Akwa Ibom state, led by LONGi Green Energy, followed by Beijing Haoyang Cloud&Data Technology’s $2.2 billion investment in a 300MW data center in Rayong, Thailand.

New M&A transactions by Chinese firms totaled $4.2 billion, a decline of 28% compared to previous quarter. Two mega transactions drove investment: Tencent’s planned $1.3 billion purchase of a 25% stake in a new subsidiary of video game developer Ubisoft in France and HongShan Capital’s $1.2 billion bid for a major stake in Sweden-based audio equipment maker Marshall Group, the first major Chinese private equity transaction in Europe since Hillhouse Capital’s $3.7 billion acquisition of Philips’ appliance unit in 2021.

The first quarter saw several notable transaction status updates. Asia Potash broke ground on its $1.6 billion industrial complex for phosphate fertilizers in Egypt. In Kazakhstan’s Atyrau region, Sinopec and its Kazakh and Russian partners began construction of a $7 billion polyethylene plant. In Scotland, China-owned Red Rock Power and ESB's Inch Cape Offshore Windfarm reached financial close and have commenced offshore construction. CALB broke ground on its EV battery plant in Sines, Portugal, committing an investment of $2.1 billion initially announced in 2022. In Mexico, Allied Machinery commenced construction of its machined components plant in Marín with an investment of $250 million.

Troubled Chinese investments included British Steel in the United Kingdom, owned by China’s Jingye Group since 2020. Jingye struggled to maintain operations at the Scunthorpe plant and halted production, prompting the closure of the UK’s last two blast furnaces. The UK government subsequently enacted emergency legislation to assume control of the company and ensure continued operations, noting that this episode has seriously affected trust in Chinese investors. In the United States, Envision AESC reportedly paused its $1.5 billion expansion of a second EV battery plant in South Carolina. Similarly in Australia, Tianqi Lithium will cease all works at one of its lithium hydroxide plants in Western Australia due to financial challenges. CNOOC completed the divestment of its Gulf of Mexico oil assets for $2 billion. In Czechia, authorities blocked a proposed investment by Beijing-based satellite firm Emposat, which planned to install a 7.3-meter parabolic antenna in the village of Vlkos. Citing national security concerns and potential espionage risks, the move marked the first use of the country’s foreign investment screening law to prohibit a transaction. The European Commission also reportedly launched a preliminary investigation into whether BYD received unfair subsidies to support its EV plant in Hungary, raising concerns over market distortion. Meanwhile, Niger’s military government expelled three Chinese oil executives from China National Petroleum Corporation, the West African Oil Pipeline Company, and the joint venture oil refinery SORAZ for allegedly violating labor and investment obligations, citing inequitable pay and unmet commitments.

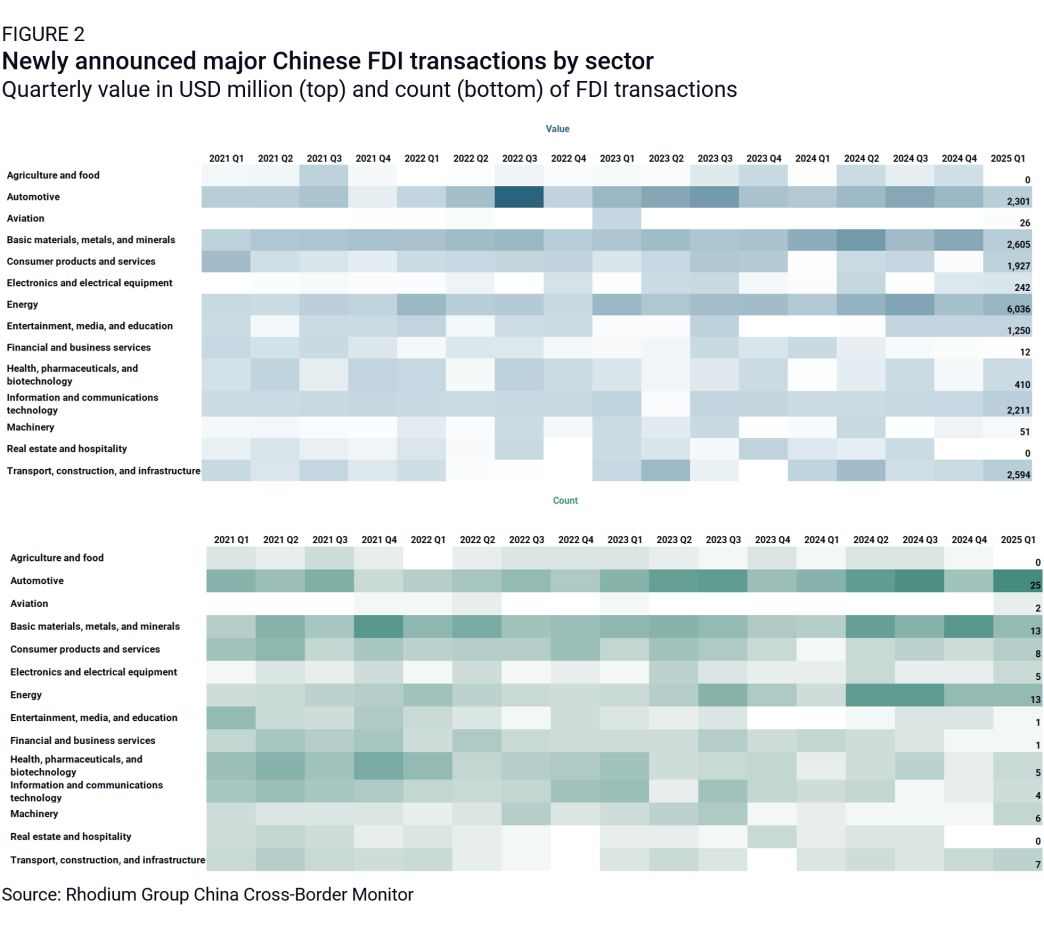

Investment by sector

Chinese outbound investment in the first quarter of 2025 was heavily concentrated in the energy, basic materials, and infrastructure sectors. The automotive industry fell out of the top three despite the announcement of a $1 billion EV battery plant by Sundowa in Thailand.

The energy sector took the top spot, attracting $6 billion across 13 major investments. The biggest transaction was LONGi Green Energy’s $4 billion green hydrogen project in Nigeria. Other notable energy transactions included Sinomach’s $996 million pumped storage power station in Cambodia and a $497 million waste-to-energy plant awarded to Shanghai SUS Environment under a concession contract in Baghdad, Iraq.

Basic materials, metals, and minerals took second place, with new investments totaling $2.6 billion. The largest project was XinFeng’s $1.7 billion manufacturing complex in Egypt, which is expected to produce automobiles, engineering equipment, and household appliances. JCHX Mining announced a $751 million expansion of its Lonshi copper mine in the Democratic Republic of Congo, while Rianlon disclosed plans for a $300 million chemical facility in Malaysia to manufacture polymer additives.

Utilities and infrastructure ranked third, with $2.6 billion in announced investment. PT China Harbour Indonesia, a subsidiary of China Communications Construction, will participate in the development of Indonesia’s new capital, Nusantara. The company is set to build and operate transport infrastructure under a public-private partnership, including multi-utility tunnel, in a project for an estimated of $1 billion. In Kuwait, China Communications Construction was tasked with implementing and managing key components of the $604 million phase of the Mubarak Al-Kabeer Port project. Meanwhile, in Brazil, China Merchants acquired a 70% stake in terminal operator Vast Infraestrutura, based at the Port of Açu, for $716 million.

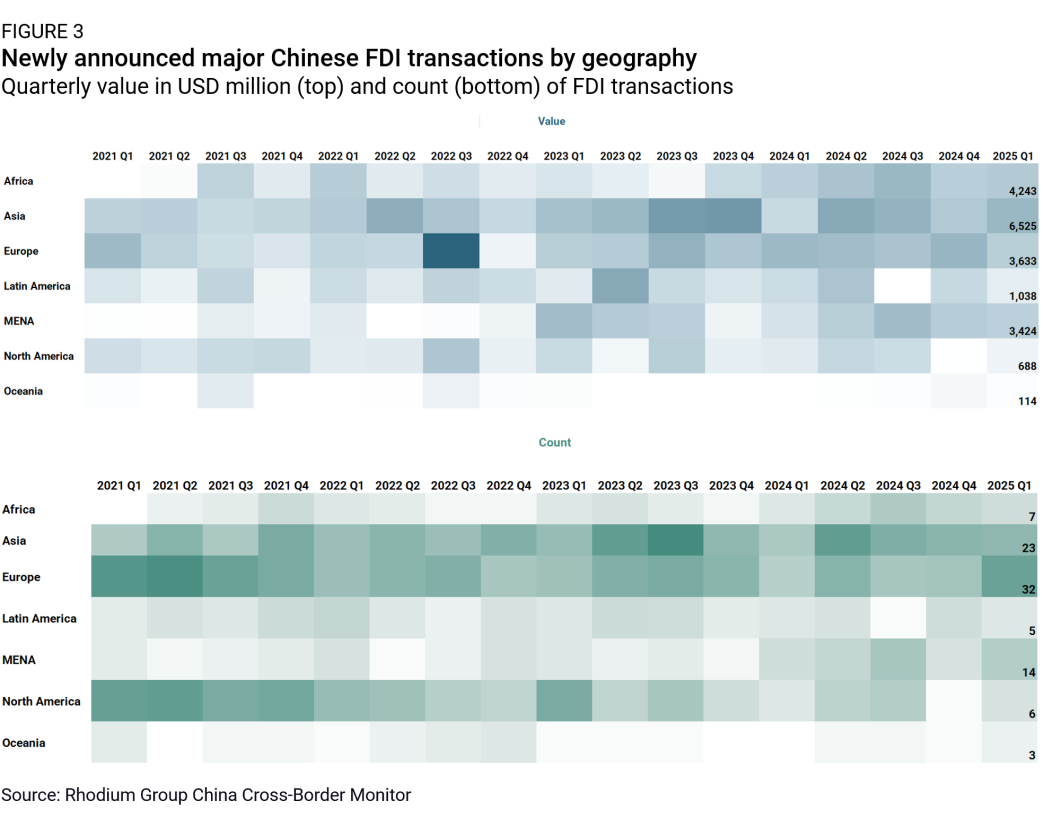

Investment by geography

As in previous quarters, Asia remained the leading recipient of new Chinese outbound investment, followed by Sub-Saharan Africa and Europe. The Middle East and North Africa (MENA) region slipped to fourth place.

Asia attracted $6.5 billion in new investment. The largest transaction was Beijing Haoyang Cloud&Data Technology’s $2.16 billion data center project in Thailand. Also in Thailand, Sundowa secured approval for a $1 billion electric vehicle battery plant—the first such facility in the country. Meanwhile, China Communications Construction committed approximately $1 billion to transport infrastructure in Nusantara, the future capital of Indonesia.

Sub-Saharan Africa followed with $4.2 billion in new Chinese investment including LONGi Green Energy’s $4 billion green hydrogen project in Nigeria; JCHX Mining’s $751 million expansion of its Lonshi copper mine in the Democratic Republic of Congo; and Canmax Technologies’ $170 million investment in two lithium mines in Nigeria.

Europe ranked third, attracting $3.6 billion in new investment. Two major acquisitions accounted for 80% of the total: Tencent’s planned $1.3 billion purchase of a 25% stake in a Ubisoft subsidiary in France, and HongShan Capital’s $1.2 billion bid for a stake in Sweden’s Marshall Group. Smaller greenfield transactions were recorded in Central Europe’s electric vehicle supply chain, including Xinzhi Group’s $136 million EV components plant in Hungary.