Dec 12, 2024Armand Meyer, Danielle Goh, Ben Reynolds, Thilo Hanemann

OECD countries have overhauled their investment screening regimes, effectively curbing unwanted Chinese acquisitions of advanced semiconductor companies. M&A activity has slowed significantly under heightened regulatory scrutiny. However, Chinese companies are expanding again in Northern Europe and Southeast Asia through greenfield FDI, which may complicate US efforts to get Chinese entities out of supply chains and curb their access to advanced technologies.

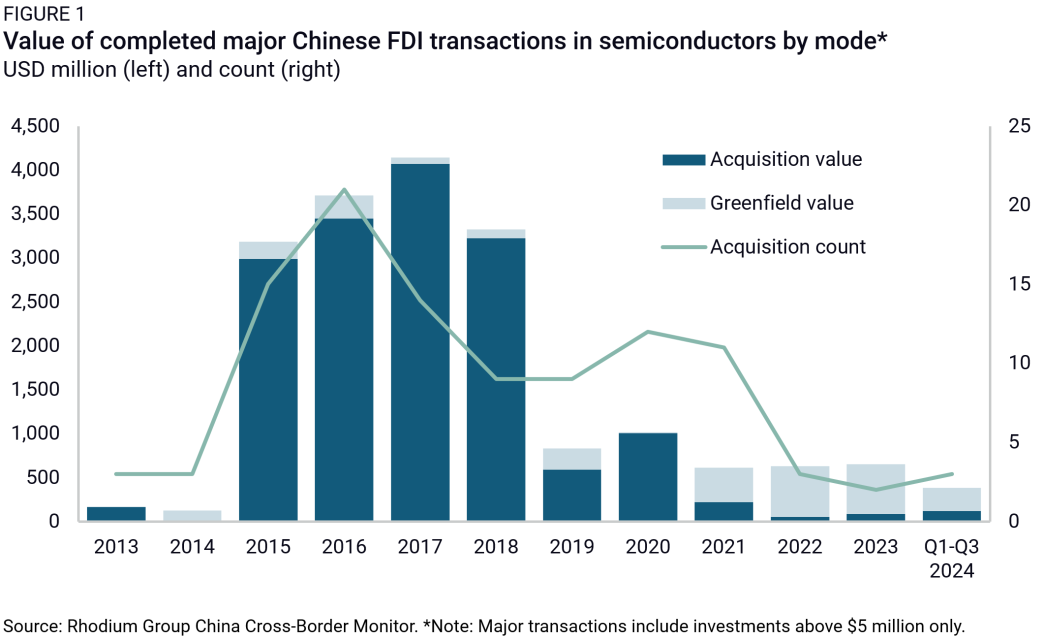

A decade ago, ample capital and Beijing’s policy guidance to acquire overseas technology triggered explosive growth in China’s outbound semiconductor investment. Chinese firms approached almost every major global semiconductor firm for potential takeovers and launched tens of billions of dollars worth of acquisitions in 2015 and 2016. Many of these transactions were withdrawn or formally blocked by regulators, but Chinese firms managed to complete around $14 billion worth of acquisitions between 2015 and 2018, including prominent chip designers and front-end manufacturers in Europe and North America such as Nexperia (Netherlands, $2.7 billion), Lixens (France, $2.6 billion), and Omnivision (US, $1.9 billion).

Since 2017, new Chinese outbound investment in the semiconductor industry has dropped off significantly as chips have come into the spotlight of US-China technology competition. As overseas regulators increased their scrutiny of Chinese high-tech takeovers, Beijing decided to direct its efforts toward nurturing domestic capacity and reducing reliance on overseas suppliers.

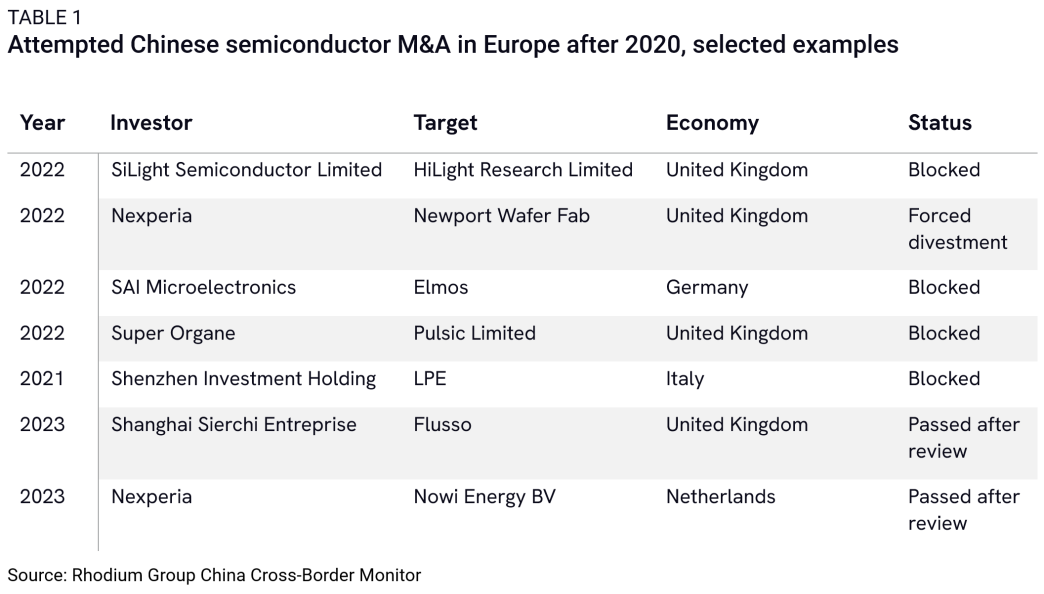

Chinese acquisitions in the semiconductor sector have not entirely ceased but are subject to intense political scrutiny and are frequently blocked by regulators (Table 1). In the US, the combination of investment screening, export controls, and supply chain security policies was effective in deterring new Chinese M&A in the semiconductor industry. Transactions that do gain approval tend to target smaller, less strategic companies or assets, primarily located in Western Europe and developed Asia. Notable examples include JECT’s acquisition of a testing facility in Singapore in 2021 and Focuslight’s acquisitions of MicroTech’s micro-optics business and OSRAM’s optical component assets in Switzerland in 2024.

Chinese overseas manufacturing booms

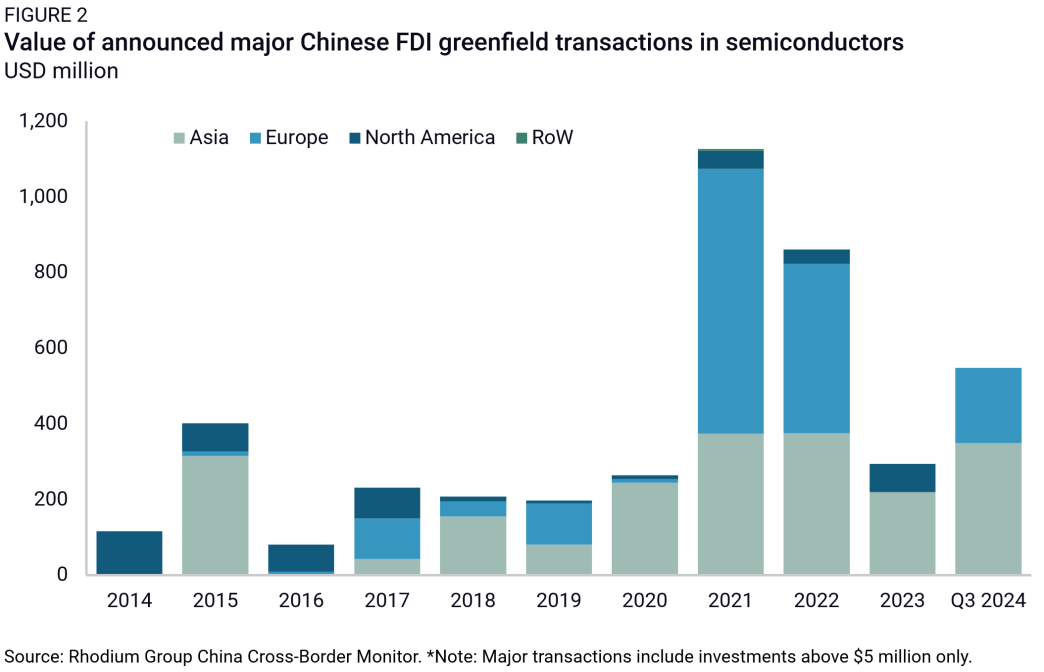

However, Chinese global semiconductor investment has seen a resurgence through organic greenfield FDI. New greenfield investment has tripled from an average of $225 million per year from 2017 to 2020 to $700 million annually since 2021, with a focus on Northern Europe and Southeast Asia (Figure 2).

In Europe, greenfield FDI has been driven by the recent expansion of local entities acquired between 2016 and 2019. After acquiring Finnish silicon wafer manufacturer Okmetic in 2016, the National Silicon Industry Group expanded the company’s front-end manufacturing capabilities between 2019 and 2021. In 2022, it announced the construction of a new $422 million wafer plant in the country, marking the first semiconductor facility built by a Chinese company in Europe. Similarly, Nexperia, acquired by Wingtech in 2018, announced several expansions totaling $900 million starting in 2021 for its manufacturing sites in Hamburg, Germany and Manchester, UK.

Other OECD economies have not experienced comparable levels of greenfield expansion, despite the presence of several Chinese-owned chipmakers. While some manufacturers have not reported significant capacity expansions outside China, the situation is less clear for semiconductor designers. For instance, Omnivision, acquired by China's Will Semiconductor in 2019, increased the number of its R&D centers by 25% with two new facilities in 2021 and 2022 without providing details regarding the capital expenditure or capacity.

In Southeast Asia, investment is driven by China+1 diversification. To reduce exposure to China and ensure continued access to key foreign customers, Chinese companies are expanding to Malaysia, Thailand, Vietnam, and Singapore. Chinese companies specializing in outsourced semiconductor assembly and test (OSAT) and integrated device manufacturing (IDM) such as TongFu Microelectronics, JCET, and Yangzhou Yangjie Electronics are leading investors, along with diversified companies like Nexperia. Malaysia stands out as a top destination, attracting 65% of the total semiconductor investment in the region. The country has become a hub for a broad range of global semiconductor firms, including American and European multinationals like Micron, Intel, and Infineon. Chinese suppliers are following these customers.

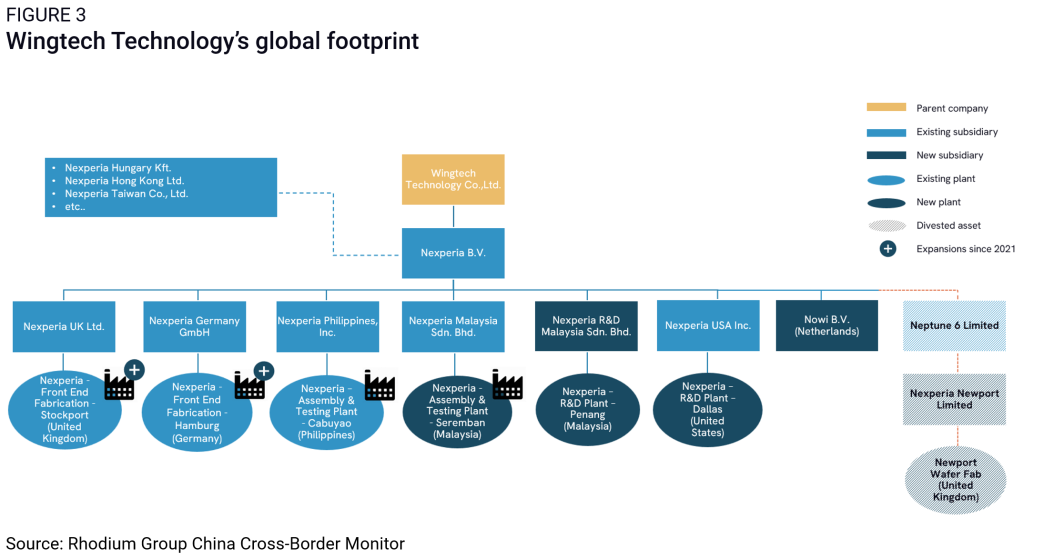

A deeper dive into Nexperia illustrates the importance of acquired entities for global expansion. Nexperia was acquired by Wingtech in 2018. Three years later, Nexperia acquired Newport Wafer Fab in Wales through a holding company, though it was later required to divest again by the UK government. In the same year (2021), it announced expansions for its manufacturing sites in Germany, the UK, and Malaysia with a total investment of more than $1 billion. It also set up new R&D plants in Dallas, Texas and Penang, Malaysia. In 2024, Nexperia announced a further $200 million expansion of its Hamburg production facility (Figure 3).

China’s overseas manufacturing push: The next G7 target?

The continued expansion of Chinese packaging and testing companies in Southeast Asia may complicate US efforts to get Chinese entities out of supply chains and curb their access to advanced technologies. Any attempt by US regulators to disrupt China’s ability to provide advanced packaging services via their Malaysian facilities would risk disproportionately impacting the businesses of major G7-based chip companies like AMD, which relies on the Malaysian facilities of its Chinese OSAT partner Tongfu Microelectronics for a significant share of its back-end assembly, test, and packaging.

However, the incoming US administration has signaled a willingness to raise tariffs on third countries that Chinese companies are using to evade direct tariffs on China. President-elect Donald Trump has announced plans to impose substantial tariffs on imports from Mexico, which, like Malaysia, benefits from Chinese export-oriented manufacturing investments. In response, Malaysian authorities hinted at their concerns they will potentially be targeted next.

Chinese-owned companies operating in OECD countries and their advanced manufacturing facilities may also come under the scrutiny of regulators under the guise of strengthening supply chain resilience. G7 countries could potentially target Chinese-owned assets in legacy chip manufacturing, with measures including forced divestments on national security grounds.

In the last round of chip export controls, the US demonstrated a growing commitment to hindering China's acquisition of foreign semiconductor assets to serve its chip self-reliance campaign. On December 2, 2024, the US Department of Commerce added JAC Capital, Wise Road Capital, and Wingtech Technology to its Entity List, citing their role in "aiding China’s government’s efforts to acquire entities with sensitive semiconductor manufacturing capabilities." JAC Capital and Wise Road Capital, two private equity firms with close ties to the Chinese government, have played a significant role in overseas semiconductor investments, notably acquiring Nexperia for $2.3 billion in 2017, which was later sold to Wingtech Technology.