A Closing Back Door? China’s Evolving FDI Presence in Mexico

Oct 10, 2024Armand Meyer, Danielle Goh, Thilo Hanemann

Although it represents a relatively small portion of total foreign investment, Chinese FDI in Mexico is significantly higher than shown in official statistics. Tariff avoidance and supply chain diversification have driven a boom in Chinese investment, first in electronics and consumer goods and lately in the automotive sector. However, a growing gap between announced and completed investments hints at growing uncertainty around Mexico's continued role as a back door to the US market.

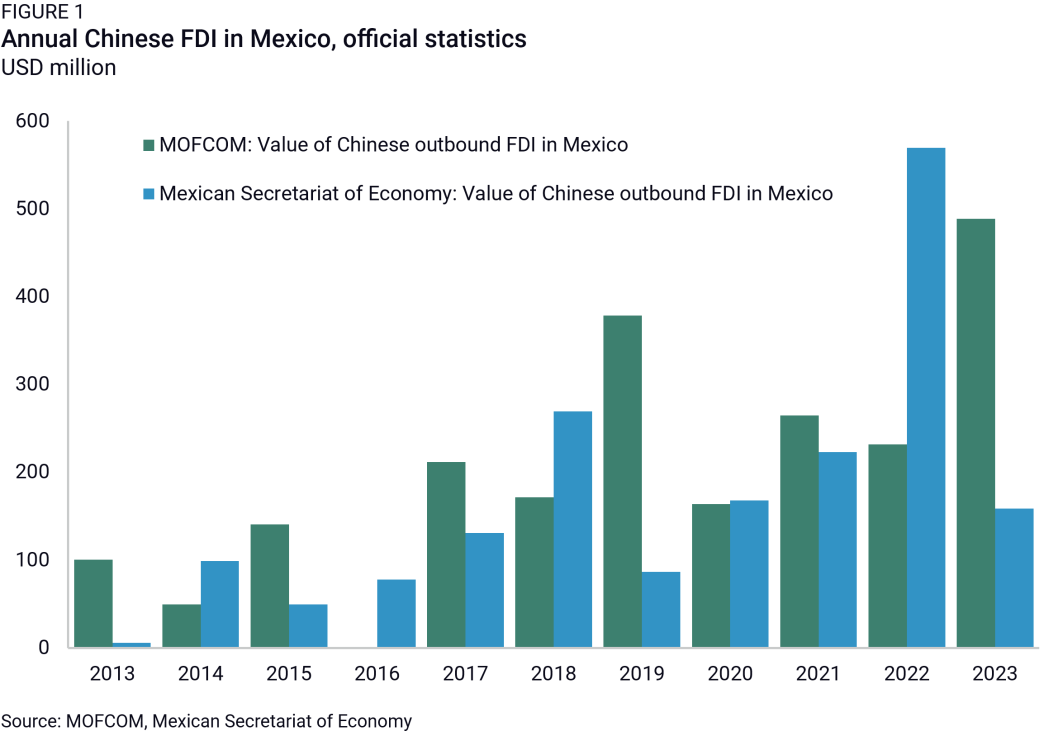

Official statistics show a modest stock of Chinese FDI in Mexico. In 2023, Mexico’s Secretariat of Economy showed a stock of $1.2 billion of investment from Chinese companies and China’s Ministry of Commerce (MOFCOM) recorded $1.7 billion. The same statistics also show only a modest increase in Chinese FDI in Mexico over the past five years (Figure 1). Starting from a low base, annual inflows averaged only $280 million from 2020 to 2023 according to Mexico’s official numbers, accounting for less than 1% of total FDI over that period. MOFCOM data presents a similar picture, with inflows averaging $290 million annually since 2020, though the annual patterns diverge from Mexican statistics.

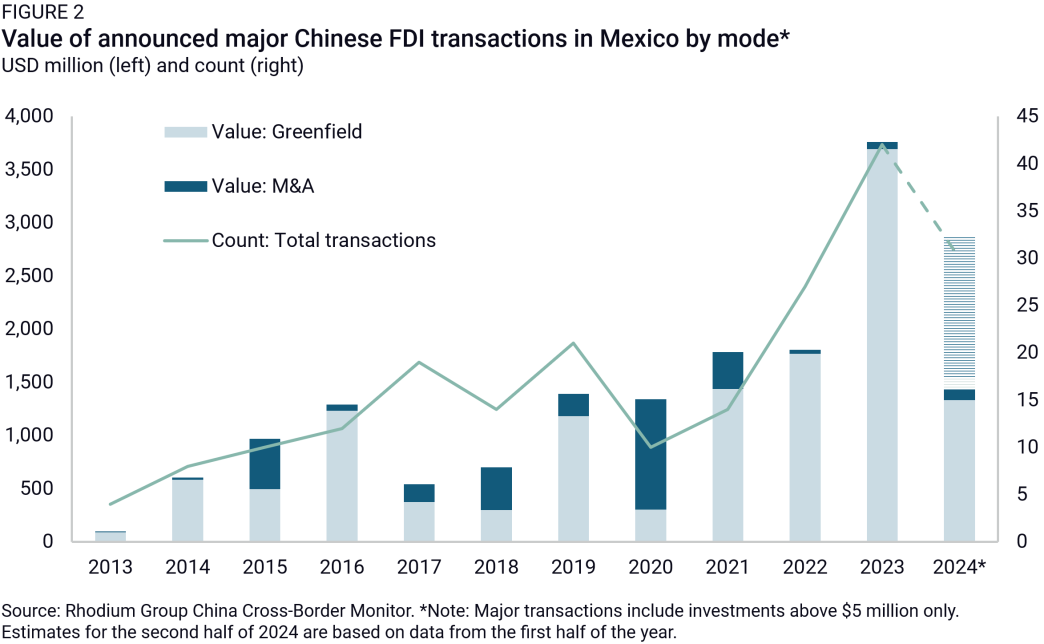

Transactions data from Rhodium Group's China Cross-Border Monitor (CBM) shows higher levels of Chinese investment. Our CBM data counts more than 700 completed FDI transactions worth a combined $13 billion. This is more than six times the official stock figures and reflects well-known gaps and distortions in balance of payments FDI data, such as investments through offshore entities in Hong Kong and elsewhere.

Our data also captures a much steeper increase in new activity over the past five years (Figure 2). Newly announced investment has continuously increased since 2014, averaging 13 major transactions per year worth an average total of $1 billion through 2020. Since 2021, we are recording another uptick in both transaction count and value, reaching 42 transactions, together worth $3.77 billion in 2023. This year is on track for similar levels, with 12 transactions, together worth $1.43 billion, in the first six months of the year. Much of this recent increase has been driven by greenfield investment, with M&A activity almost vanishing after 2021.

A backdoor to the US?

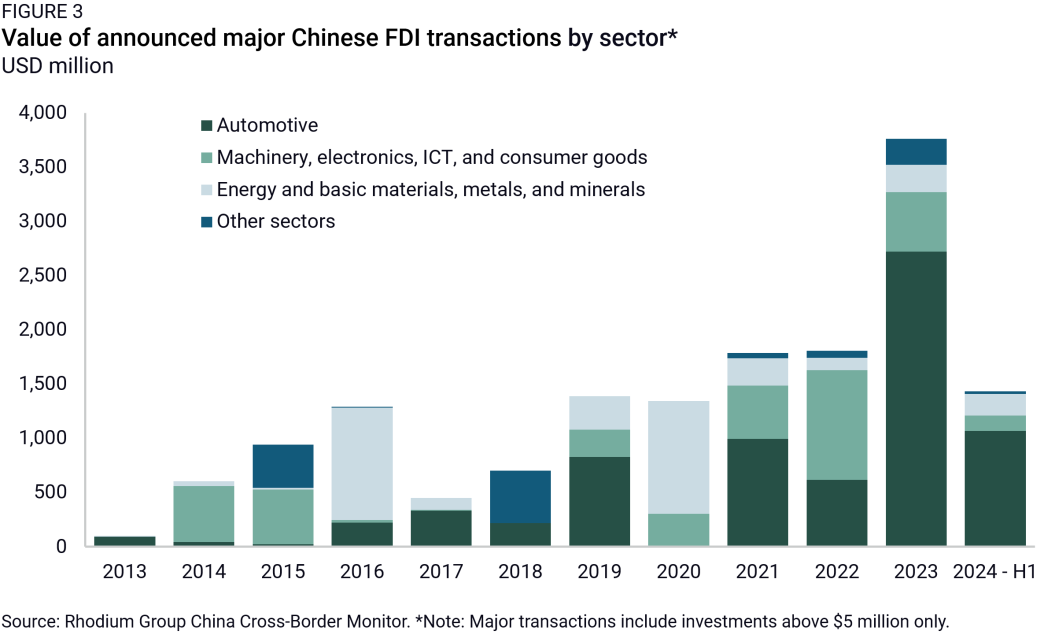

The CBM's transaction-based approach to FDI lets us dissect the drivers and industry composition of Chinese investment in Mexico (Figure 3). Mexico became a major US trade diversification hub in the wake of tariffs under the Trump administration (see Full Circle: Mexico’s Resurgence Amid US-China Trade Frictions), so it does not come as a surprise that tariff-hit electronics and consumer goods manufacturing—represented by companies like Lenovo, Hisense, and Man Wah—have been significant contributors, accounting for 30% of the total announced value over the past five years.

The automotive sector has long been another major driver of Chinese (and foreign) FDI in Mexico, accounting for about a third of investment in Mexico since the mid-2010s. In the past few years, however, it has become the predominant driver of investment. In 2023, Chinese companies announced automotive investments worth $2.72 billion, representing 72% of Chinese investment in the country that year. This trend continued into the first half of 2024, with automotive investments making up three quarters of the total.

This growth is largely dominated by parts manufacturers, such as ZC Rubber, which announced a $600 million investment in 2024. Major US and European car manufacturers like Tesla and BMW are driving a broader automotive FDI boom in Mexico, predicated on access to the US market via the US-Canada-Mexico (USMCA) trade agreement. Chinese suppliers are following them abroad.

Chinese battery makers and car manufacturers have remained more cautious, however. Companies like BYD, Chery, and BAIC have expressed interest in establishing factories in Mexico but have yet to make concrete commitments. CATL announced plans to build a battery factory but paused those efforts in 2022 due to concerns over US restrictions on sourcing materials used in EV batteries under the Inflation Reduction Act.

Mexico’s energy and materials sector has also attracted significant interest for M&A activities. Ganfeng Lithium completed the acquisition of the Sonora lithium mining project for $391 million in 2021, and China Power purchased the renewable energy projects developer Zuma Energía. However, greenfield developments in these sectors have faced setbacks. CNOOC has yet to start commercial operation of its oil blocks within the Cinturon Plegado Perdido basin and Ganfeng’s plans to develop its lithium project have been halted following the cancellation of its mining concession by authorities.

Policy uncertainty looms

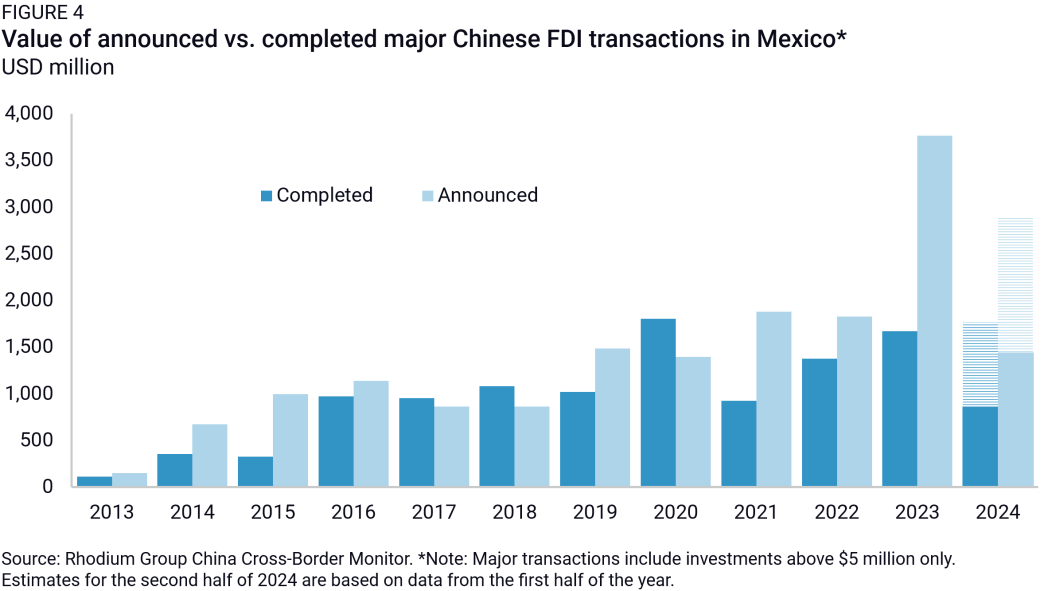

While some Chinese firms are eyeing the local Mexican market, overall investment appetite will be shaped by market access to the US. The Inflation Reduction Act’s sourcing restrictions and new tariffs on Chinese EVs imposed by the Biden administration have already led to a growing gap between announced and completed investment by Chinese firms (Figure 4), suggesting a wait and see attitude among Chinese investors.

Last week, the US Commerce Department proposed new rules banning the use of certain Chinese software and components in vehicles. In practice, these rules would forbid the import of Chinese cars and certain auto parts to the United States altogether. For certain Chinese auto parts makers supplying non-Chinese carmakers in Mexico, these rules could kneecap the business rationale for new investments there.

The upcoming US presidential election in November could further increase hurdles to all auto imports from Mexico. Republican candidate Donald Trump announced that he would impose tariffs of 100% on cars imported from Mexico in an effort to encourage manufacturing in the United States. In June, Tesla paused plans to build a factory in Mexico until after the election. A permanent slowdown of foreign auto investment in Mexico would in turn crimp Chinese investment in auto parts, putting around $2 billion of announced Chinese investment in the auto parts industry at risk.

The upcoming joint review of the USMCA trade agreement stands to further complicate Chinese companies' corporate footprint in Mexico. The agreement is up for renewal in July 2026, and China will be a growing factor in these negotiations. A bipartisan group of four senators specifically called out Chinese investment in Mexico as a problematic backdoor to the US market and called for action to prevent it. Mexico's newly elected president will have to balance economic growth provided by Chinese investments with US concerns over them. Washington could use the renewal process of the USMCA to try to compel Mexico to condition or block Chinese investment, increasing uncertainty in the business environment and further eroding Chinese investments there.