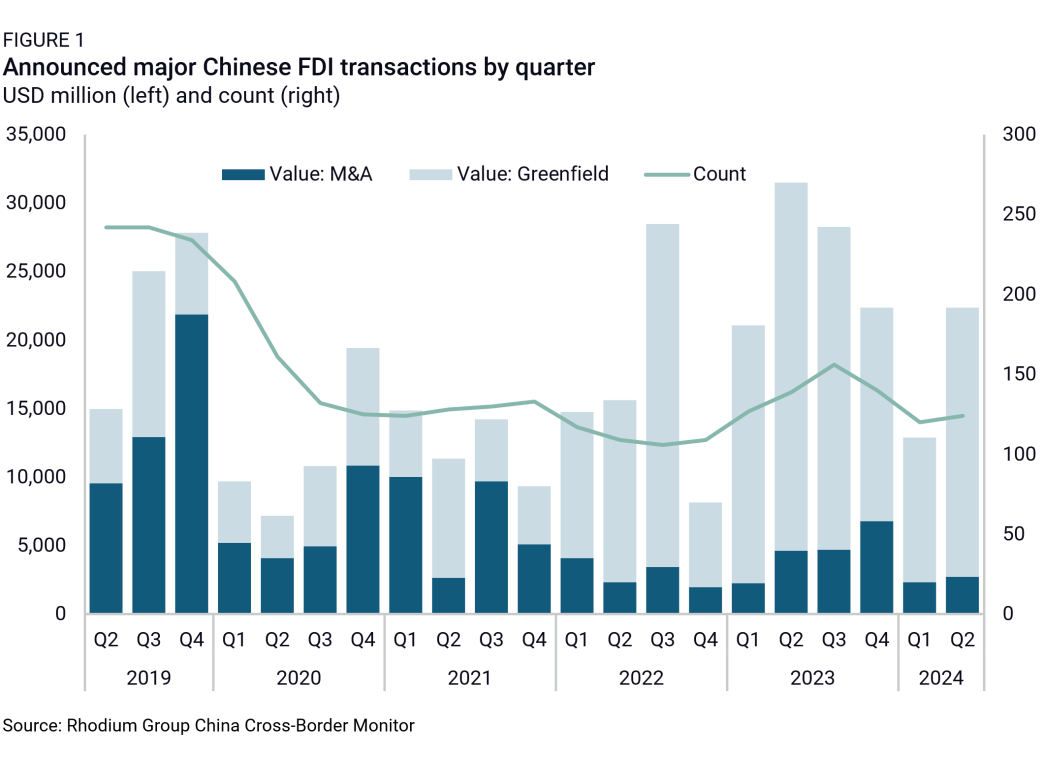

After a notable post-COVID rebound, China’s outbound foreign direct investment is losing steam again. Investment in Q2 rebounded slightly from the previous quarter but H1 activity remained lower than the same period of 2023. Asia and Europe remained the top recipient regions of Chinese capital, driven by investment in the automotive, basic materials, and power generation sectors.

The 2023 post-COVID outbound investment boom from pent-up demand seems to be subsiding somewhat, as further growth is being constrained by economic and political realities. In Q2 2024, we recorded 167 announced major outbound foreign direct investment (OFDI) transactions by Chinese companies worth an estimated $22.38 billion. This represents a small rebound in volume terms and a 74% increase in value terms from the first quarter. For the first half of the year, we count 260 new investments worth $35.28 billion, down from 312 investments worth $52.57 billion in the same period of 2023.

Greenfield projects have remained in the driving seat, accounting for 88% ($19.64 billion) of newly announced OFDI in Q2 2024. Four multi-billion-dollar deals accounted for 40% of the total value: A $2.4 billion oil processing plant in Serbia announced by China Energy, a $2.3 billion polyethylene plant by Sinopec, a $1.75 billion steel plant in Kazakhstan by Fujian Hengwang, and a $1.13 billion EV battery plant in South Carolina by Envision AESC.

Mergers and acquisitions (M&A) activity, on the other hand, reached one of its lowest levels since Q1 2023 with only 40 announced transactions worth $2.75 billion. Midea’s acquisition of Arbonia’s climate business in Switzerland for $820 million was the top transaction, followed by Ganfeng Lithium’s stake increase in the Goulamina lithium mining project in Mali for $342 million.

Notable status updates in Q2 include the completion of Enel’s $ 3.10 billion acquisition of assets from China Southern Power Grid in Peru. Canceled transactions include Svolt’s second battery factory in Germany and the public auction for the unfinished Oceanwide Plaza in downtown Los Angeles. Governments intervened in several transactions, with Germany blocking the sale of Volkswagen's gas turbine business to China, the US government ordering a Chinese crypto miner to sell land near a US military base, and Australia mandating the disposal of China-linked shares in Northern Minerals. Disputes include a challenge to Ganfeng Lithium concessionary rights in Mexico, a conflict between Tianqi Lithium and a local state-owned enterprise in Chile, and the Peruvian government's move to revoke COSCO's exclusive right to operate the port of Chancay.

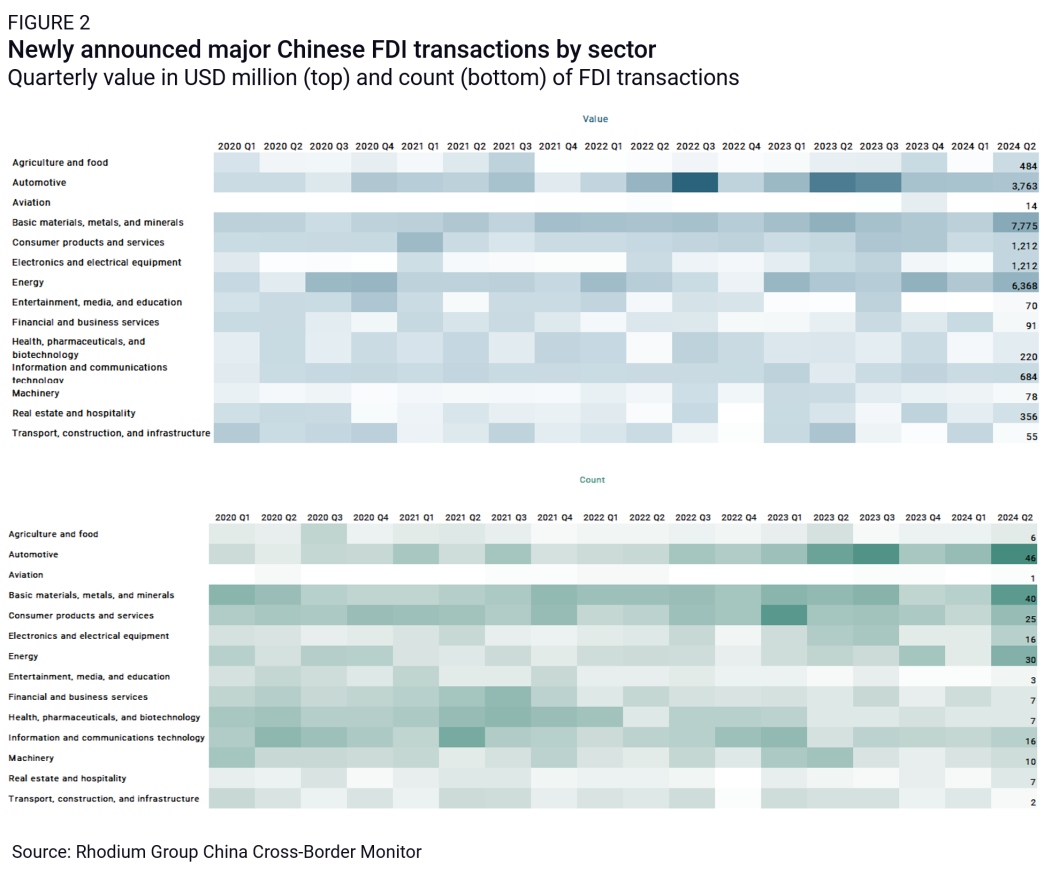

Investment by sector

Chinese outbound investment in Q2 remained concentrated in a handful of industries, continuing a trend from previous quarters.

Basic materials, metals, and minerals investments topped the quarter with a total of $7.78 billion (35% of Q2 value). Two greenfield projects in Kazakhstan account for the lion’s share of that investment: Fujian Hengwang Investment's $1.75 billion investment in a steel plant and Sinopec’s $2.3 billion chemical plant.

The energysector accounted for $6.37 billion in investment (28% of total Q2 value). China Energy’s oil refinery accounts for around 40% of that, followed by $2.40 billion of investment in solar and wind power generation and $1.38 billion in renewable energy equipment manufacturing.

Investment in the automotive sector remains strong at $3.76 billion (17% of Q2 value), largely driven by manufacturing projects in the EV supply chain. The largest auto investment this quarter was Envision AESC’s announced $1.13 billion expansion of its existing plant in South Carolina. Aside from auto suppliers, Chery announced its first two electric vehicle manufacturing plants in Southeast Asia, with plants in Thailand ($400 million) and Vietnam (estimated $160 million).

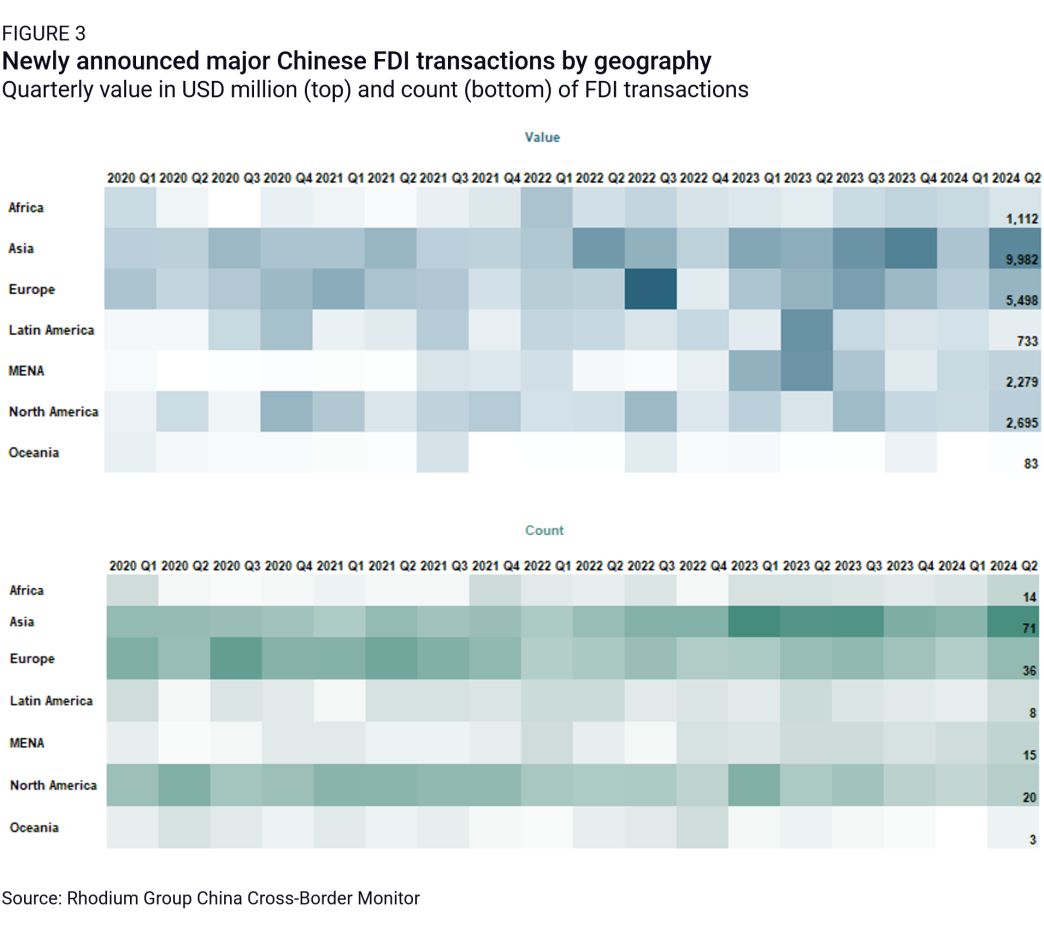

Investment by geography

Asia and Europe remain the top recipients of Chinese outbound investment.

With $9.98 billion, Asia accounted for 45% of new investment in Q2. Southeast Asia continues to be the biggest draw for Chinese investors, accounting for around 46% of China’s investment value in Asia. Fujian Hengwang and Sinopec plants made Kazakhstan the top recipient country of the region. Vietnam also stands out, with Chery’s EV plant and the Victory Giant PBC plant. Indonesia continues to be a favored destination, bolstered by Hongshi Cement’s $622 million cement plant.

Europe attracted $5.50 billion worth of new investment in Q2 (25% of total). Serbia recorded the largest transaction in the quarter with China Energy International Group’s $2.4 billion oil processing plant. It also landed three other projects: a solar power plant, a solar panel factory, and a steel plant. Europe also attracted the largest M&A deal this quarter, with Midea Group’s $820 million acquisition of Arbonia’s climate division in Switzerland.

North America has seen elevated investment in recent quarters, attracting $2.7 billion of new investment in Q2 (12% of total). The United States was the top recipient with Envision’s $1.13 billion expansion in South Carolina, Shenzhen Capchem Technology’s battery factory in Louisiana for $350 million, and Boviet Solar’s $294 million solar modules manufacturing plant in North Carolina. Mexico was another major recipient with Eaglerise’s $189 million solar electric transformer plant in Coahuila and continuing activity in the automotive industry including new facilities by Sailun Tire and Minth Group.