China’s outbound FDI momentum remained elevated in Q2 2025, making the first half of the year the strongest since 2020. The basic materials sector led the surge, recording its highest level of announced investment since the onset of the COVID-19 pandemic. Investment in the automotive sector also rebounded, driven by a new wave of investments in the electric vehicle supply chain. Africa surpassed Asia and MENA as the top destination for announced investment, though the completion rate of announced investment is historically lower there than in other regions. There is still little evidence that elevated trade barriers have triggered significant shifts in manufacturing outbound investment.

Investment momentum

Updated data from the China Cross-Border Monitor (CBM) shows 135 major FDI transactions by Chinese companies in Q2 2025 totaling an estimated $27.1 billion. The first six months of 2025 mark the strongest half-year for Chinese FDI since the onset of COVID-19.

Greenfield investment remained the dominant mode of entry for Chinese outbound investment, totaling $23.1 billion and accounting for 85% of total investment. Mega transactions over $1 billion account for 58% of the total investment. The largest project was a $7 billion investment from China’s Hunan Sunwalk Technology Group in a titanium extraction and processing facility in Malawi, but there are doubts about its feasibility (see below).

New M&A transactions by Chinese firms totaled $4.0 billion, falling by 24% compared to the previous quarter and continuing a slowdown since Q4 2024. In contrast to Q1 2025, no billion-dollar acquisitions were announced in Q2. In Singapore, Zhejiang Longsheng Group completed a $696 million transaction to take full ownership of chemical manufacturer DyStar. China’s CMOC Group announced it would acquire Lumina Gold in a transaction valued at $421 million.

The second quarter saw several notable transaction status updates. In Kazakhstan, Sinopec and a Russian joint venture partner broke ground on a $3 billion polyethylene complex, marking one of the largest claimed petrochemical investments in Central Asia. Zijin Mining Group finalized its acquisition of the Akyem gold mine from US-based Newmont Corporation for up to $1 billion, expanding its footprint in Ghana. In Brazil, Baiyin Nonferrous Group took full ownership of the $420 million Serrote copper mine in Alagoas. In the United States, Hithium opened a $200 million battery energy storage equipment plant in Texas. In Europe, China State Grid closed its $70 million acquisition of a 20% stake in Greece’s Ariadne Interconnection, a firm tasked with implementing the Attica-Crete submarine power transmission project. Envision has also officially started production at its billion-dollar battery gigafactory in Douai, France.

Troubled Chinese investments included Sino Minerals Investments in Uganda, where local residents have opposed a $34 million iron ore processing plant, citing inadequate compensation for land acquisition. A $660 million investment by CATL in a lithium extraction processing plant in Bolivia was halted this quarter, after a local court ruling suspended project activity. In Chile, Tsingshan and BYD have unexpectedly withdrawn from their planned lithium cathode manufacturing projects. In the United States, AESC has paused construction of its $1.6 billion electric vehicle (EV) battery plant in South Carolina. The company attributed the delay to rising economic uncertainty and demand-side volatility. Geely and BYD have reportedly faced delays in securing Beijing’s approval for new project expansions in Latin America.

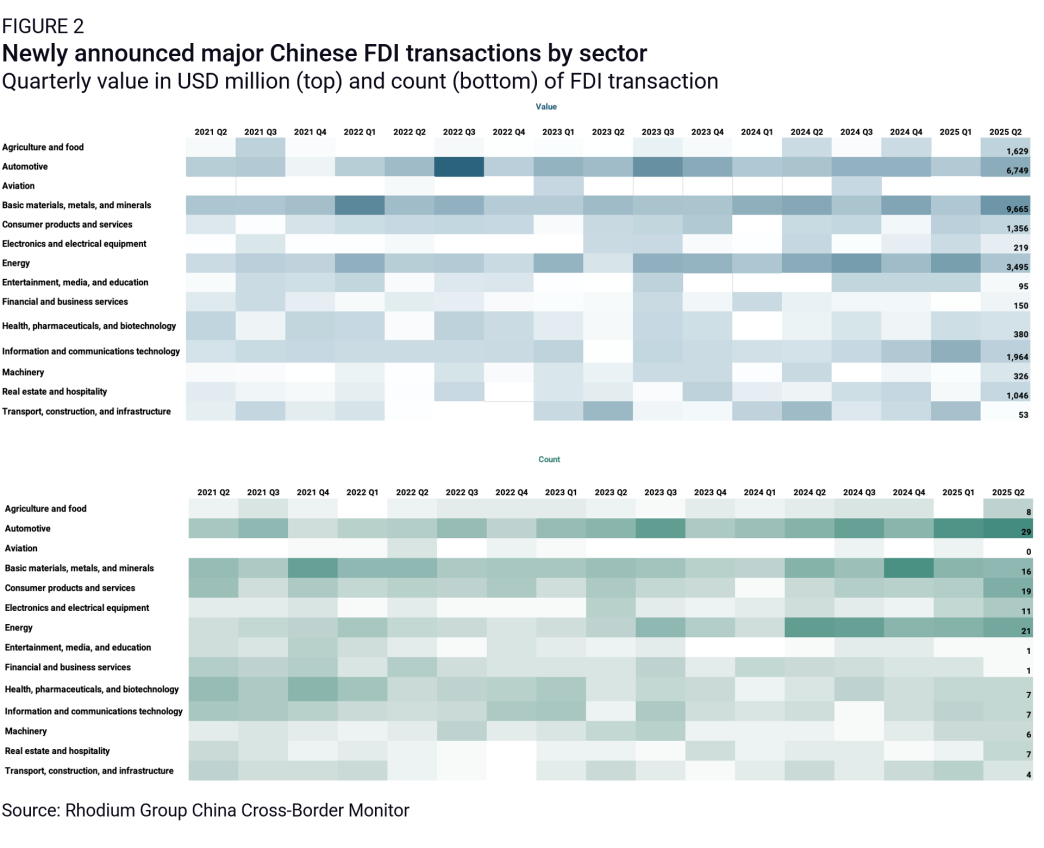

Investment by sector

The top recipients for Chinese outbound investment in Q2 2025 were basic materials, automotive and energy sectors.

The basic materials, metals, and minerals sector ranked first, attracting $9.7 billion in investment, the highest quarter since COVID-19. The largest project was a $7 billion agreement between the Government of Malawi and China’s Hunan Sunwalk Technology Group for a titanium extraction and processing facility, signed during the China-Africa Economic and Trade Expo in Changsha. However, the project specifications are rare and observers have voiced doubts that the project will materialize. In Singapore, Zhejiang Longsheng Group acquired the remaining 37.57% stake in DyStar Global Holdings, a global specialty chemical and dyestuff manufacturer, from Kiri Industries for $697 million, making DyStar a wholly-owned Chinese subsidiary. The sector also saw a $500 million investment by Jingdong Steel in a steel production facility in Algeria’s Dhraa El-Hadja industrial zone.

The automotive sector came in second place, attracting $6.8 billion across 29 major investments. Just two transactions accounted for 56% of total investment value: Huayou Cobalt announced to invest $2.0 billion in a $8.4 billion Indonesian EV battery complex, where it is replacing South Korea’s LG Energy Solution. GAC Group announced a $1.3 billion EV facility in Goiás, Brazil. We recorded higher than usual activity by EV parts manufacturers, with eight transactions exceeding $100 million. The largest among them was led by GEM, a Chinese battery materials manufacturer, which committed $293 million to expand its ternary precursors facility in Indonesia.

The energy sector ranked third and only saw $3.5 billion in investment, down from its record 2024 quarterly average of $5.9 billion. The largest transaction was led by Geo-Jade Petroleum, a Chinese oil and gas developer, which will undertake a $1.2 billion joint investment with Iraqi partner HILAL Al Basra to develop an oil and gas project in Iraq, holding a 67% stake and contributing $848 million. In Turkey, Astronergy, the solar unit of Chint Group, announced plans to build a solar cell manufacturing facility for $500 million. In Uzbekistan, China Electrical Equipment International and China Huadian Overseas established Huadian Jizzakh Solar Power LLC to build and operate a 500 MW solar power plant in the Jizzakh region, with an estimated investment of $288 million.

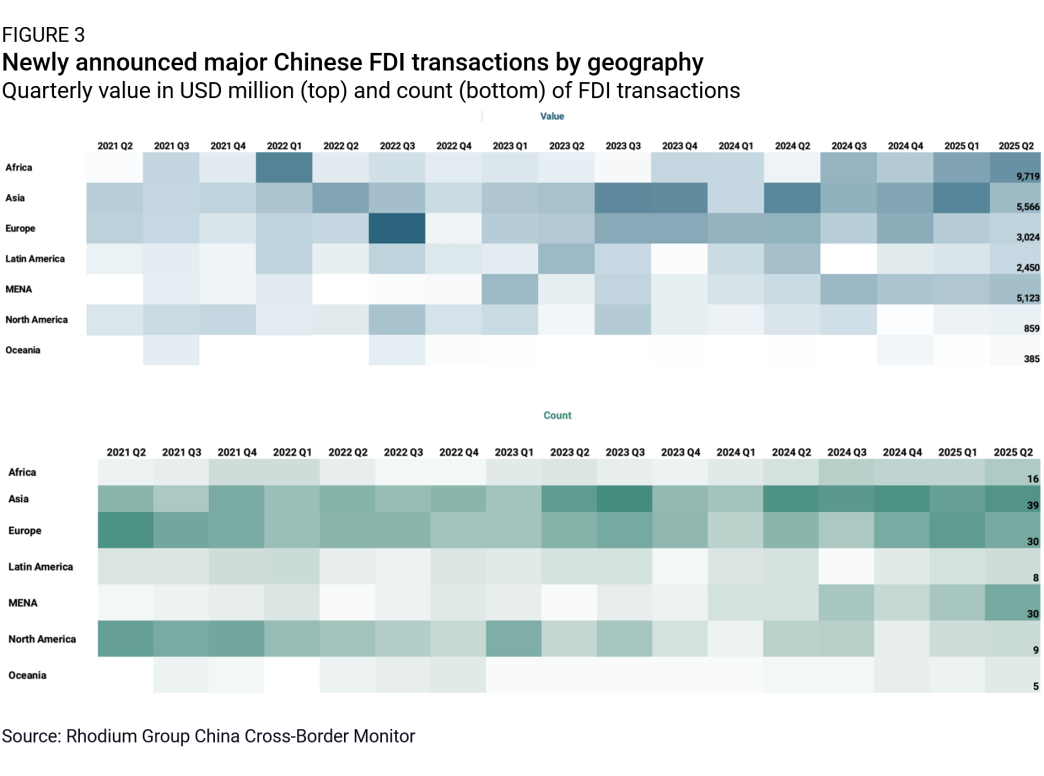

Investment by geography

Africa became the top destination of Chinese capital in Q2, followed by Asia and the MENA region.

Africa ranked first, attracting $9.7 billion in new Chinese investment. Investment has surged 57% since Q3 2024. The largest transaction was Hunan Sunwalk Technology Group’s $7 billion commitment to a titanium mining and processing project in Malawi. Sinomach is building and financing a $1 billion sugar cultivation and processing facility in Nigeria’s Kwara State. In Kenya, Zonken Group announced a $373 million investment in an aloe vera processing plant and vineyard project in Baringo.

Asia ranked second, with $5.6 billion in announced investment, though it lost momentum, returning to quarterly average levels last seen in 2021. Huayou Cobalt’s $2 billion participation in an Indonesian EV battery consortium and Zhejiang Longsheng Group’s $697 million acquisition of DyStar Global Holdings accounted for over half of the regional total. The next largest transaction was Jingxing Paper’s $400 million expansion of its kraft liner production facility in Malaysia.

The MENA region followed closely behind Asia, attracting $5.1 billion. Zhongke Electric committed $1.1 billion to build a lithium-ion battery anode material plant in Oman. In Iraq, Geo-Jade Petroleum will commit $848 million as the majority partner in a $1.2 billion joint venture with HILAL Al Basra to develop upstream oil and gas assets. In Morocco, Guangzhou Tinci Materials Technology announced a $282 million investment to establish an EV battery materials facility.